Important Tax Strategies for a Transitional and Untraditional Year-End

First and foremost, we hope that you, your family and all of your loved ones are remaining safe and healthy during this incredibly difficult year, which has been challenging on many different levels. While achieving tax savings is an important financial goal, 2020 has certainly emphasized how secondary or even tertiary of a concern this can be.

That being said, this past year has seen the passage of several significant tax laws – among them the Setting Every Community Up for Retirement Enhancement Act (SECURE Act), which we wrote about in this Alert and the Coronavirus Aid, Relief and Economic Security Act (CARES Act), which we wrote about in this Alert). The SECURE Act changed many tax rules related to retirement contributions and distributions under an individual retirement account (IRA) or 401(k), while the CARES Act utilized numerous tax and other financial provisions to inject cash into a struggling economy to assist both businesses and individuals in response to COVID-19.

As we near the end of the year, there is still time to position yourself to take advantage of the opportunities presented by the new tax acts, including identification and execution, before year-end to reduce your 2020 tax liability. Our annual Tax Planning Guide is designed to highlight notable tax provisions and potential planning opportunities to consider for 2020 and, in some cases, 2021, both with tempered caution and balance this year.

With a tumultuous election (almost) behind us, we are gaining greater clarity on what tax measures may be implemented in 2021 and beyond. Based upon current projections by major news outlets while awaiting certified results, it is likely former Vice President Joe Biden will become the 46th president on January 20, 2021.

With his election, as with any new administration, there comes the eternal optimism of an incoming party being able to make broad, systematic changes to shape the government in their image. Of course, in order to make the most ambitious changes, a party would need to control the House, Senate and presidency, as the Democrats did when passing the Affordable Care Act in 2010, and as the Republicans did when passing the Tax Cuts and Jobs Act (TCJA) in 2017. As of this writing, media outlets are projecting that the House of Representatives will remain controlled by the Democrats for the 117th Congress starting in 2021, albeit with a smaller majority than they enjoyed in the 116th Congress. Regarding the Senate, currently most outlets are predicting that Republicans will control 50 seats, as compared to the Democrats’ 48. The two remaining seats in the Senate will be decided in run-off elections to occur in Georgia on January 5, 2021.

In order for Democrats to win control of the Senate, they will need to win both of the available Georgia Senate seats, which then require Democrats to utilize Vice President-elect Kamala Harris as a tiebreaker. Even in such a scenario, for any legislation to pass by a simple majority, the Democrats would need to obtain support from their entire caucus in the Senate with no dissenters. Thus, we believe it highly unlikely that ambitious and robust or even controversial legislation will be enacted in the near term. Rather, the president and Senate will likely need to build bipartisan consensus in order to get any legislation passed, as it is likely Republicans will win at least one seat in Georgia, and therefore retain control of the Senate. With the houses of Congress split in terms of political control, legislation will need to include items attractive to members on both sides of the aisle, or at least appropriate concessions to the other side. We do believe that with the ever-increasing deficit, especially in light of the trillions of dollars being spent to deal with the COVID-19 pandemic, Congress will need to act and a tax increase may (perhaps will) be needed to a certain degree. At this moment, we envision incremental, rather than sweeping, tax changes as both a divided Congress or a razor-thin controlled Congress would leave the prospects for major tax legislation remote at best.

For example, Congress has not yet passed a fiscal year 2021 budget resolution. As a result, it is possible the new Congress could pass piecemeal tax changes under a fiscal year 2021 budget in January followed by another round of tax changes later in the year when a fiscal year 2022 budget is negotiated.

The ideological differences in the Senate suggest at least two years of gridlock. However, with President-elect Biden and Senate Majority Leader McConnell’s experience negotiating with Democrats in the House, both sides are capable negotiators and likely to get some legislation through. However, the process will not be easy or swift and we forecast change will be incremental and slow. Should Democrats gain control of the Senate in the 2022 election, tax increases would likely be swift and substantial, but both scenarios remain uncertain at this time.

Furthermore and uncharacteristically, another opportunity for tax planning may exist. Typically, the longer it takes to pass tax legislation, the harder it will become for legislators to justify an effective date retroactive to January 1, 2021. While not unprecedented, retroactive tax rate increases are relatively rare. There have been six major rate increases since 1980 and only the 1993 increases in the corporate tax rate from 34 percent to 35 percent and individual rates from 31 percent to 39.6 percent were retroactive to January 1. The 1993 bill was passed in August and made retroactive to January 1, 1993. With a divided government, compounded by a pandemic, it may be difficult to match this timeline. Interestingly, it took all of 2017 to enact sweeping tax changes and President Trump and the Republicans made tax reform a top priority.

So, while tax increases are not typically effective prior to the date a bill is first introduced in Congress, if tax legislation does manage to get traction in 2021, another planning window to execute tax strategies from early January until a formal bill is introduced in the House Ways and Means Committee may exist.

As a result, we recommend the prudent approach of planning now, based on current law, and revising those plans as the need arises.

So, please check in with us and keep a watchful eye on our Alerts, which are published throughout the year and contain information on tax developments that are designed to keep you informed of significant changes in those environments.

In this 2020 Year-End Tax Planning Guide prepared by the Tax Accounting Group (TAG) of Duane Morris, we walk you through the steps needed to assess your personal and business tax situation in light of the new laws and identify actions needed before year-end to reduce your 2020 tax liability.

We hope you find this complimentary guide valuable and invite you to consult with us regarding any of the topics covered or your own unique situation. For additional information, please contact me at 215.979.1635 or magillen@duanemorris.com, or the practitioner with whom you are in regular contact.

We wish you a joyous holiday season and a healthy and prosperous new year.

Michael A. Gillen

Tax Accounting Group

About Duane Morris LLP

Duane Morris LLP, a law firm with more than 800 attorneys in offices across the United States and internationally, is asked by a broad array of clients to provide innovative solutions to today’s legal and business challenges. Evolving from a partnership of prominent lawyers in Philadelphia more than a century ago, Duane Morris’ modern organization stretches from the U.S. to Europe and across Asia. Throughout this global expansion, Duane Morris has remained committed to preserving its collegial, collaborative culture that has attracted many talented attorneys. The firm’s leadership, and outside observers like the Harvard Business School, believe this culture is truly unique among large law firms and helps account for the firm continuing to prosper throughout changing economic and industry conditions.

In addition to legal services, Duane Morris is a pioneer in establishing in-depth, nonlegal services to complement and enhance the representation of our clients. The firm has independent affiliates employing approximately 100 professionals engaged in other disciplines, such as the tax, accounting and litigation consulting services offered by the Tax Accounting Group.

About the Tax Accounting Group (TAG)

TAG maintains one of the largest tax, accounting and litigation consulting groups within any law firm in the United States and has an active and diverse practice with over 60 services lines in more than 45 industries. To learn more about our service lines and industries served, please refer to our Quick Reference Service Guide.

TAG’s certified public accountants, certified fraud examiners, financial consultants and advisers provide a broad range of cost-effective tax compliance, planning and consulting services as well as accounting, financial and management advisory services to individuals, businesses, partnerships, estates, trusts and nonprofit organizations. TAG also provides an array of litigation consulting services to lawyers and law firms representing clients in regulatory and transactional matters and throughout various stages of litigation.

As the entrusted adviser to our clients in nearly every state in our nation and 25 foreign countries, TAG, year after year, continues to enjoy impressive growth, in large part because of our clients’ continued expressions of confidence and referrals. Our one-of-a-kind CPA and lawyer platform allows us to efficiently deliver one-stop flexibility, customization and specialization to meet each of the traditional, advanced and unique needs of our clients, all with the convenience of a single-source provider.

Our service mission is to enthusiastically provide effective solutions that exceed client expectations. What allows us to fulfill our mission and maintain long-term client relationships is the passion, objectivity and deep experience of our talented professionals. Our senior staff has an average of over 20 years working together as a team within our group (with a few having more than 30 years on our platform). These dedicated professionals, who are intimately familiar with and take a personal interest in our clients’ needs, work very hard to justify the trust placed in us.

With tax year 2020 rapidly (and for many, thankfully) coming to an end, it is time once again to consider and, where appropriate, implement year-end tax planning strategies available to you, your family and your business. With an unclear legislative future, a fragile environment due to COVID-19 and a volatile tax environment, tax-savings strategies become increasingly important and this year is no exception.

So while you can depend on TAG for cost-effective tax compliance, planning and consulting services, as well as for critical advocacy and prompt action in connection with your long-term personal and business objectives, we are also available for any immediate or last-minute needs you may have or Congress may legislate.

This year, with a lame duck Congress for the rest of the year, and both chambers of Congress likely to remain split thereafter, we do not expect sweeping tax legislation on the immediate horizon as described in our letter accompanying this planning guide. With incremental and modest tax changes likely for 2021, the tried and true strategies of deferring income and accelerating deductions may be beneficial in reducing tax obligations for most taxpayers in 2020. However, with tax increases looming, whether incremental or otherwise, the better approach may be to “time” income and deductions rather than broadly deferring income and accelerating deductions. With minor exceptions, this coming month is the last time to act for tax year 2020 to develop and implement your tax plan but it’s certainly not the last opportunity.

For example, if you expect to be in the same tax bracket in 2021 as 2020, the traditional strategies of deferring taxable income and accelerating deductible expenses can often achieve overall tax savings for 2020 and possibly for both 2020 and 2021. However, by reversing this technique and accelerating 2020 taxable income and/or deferring deductions to plan for a higher 2021 tax rate, your two-year tax savings may be higher. This may be an effective strategy for you if, for example, if you have charitable contribution carryovers to absorb, or your marital status will change next year, or your head of household or surviving spouse filing status ends this year. This analysis can be complex, and you should seek professional guidance before implementation. Examine our “Look Before You Leap” section below for additional thoughts in this regard.

For individuals, the SECURE Act pushed back the first required minimum distribution (RMD) from IRAs or defined contribution plans from age 70½ to age 72, while also removing the prohibition on IRA contributions for those over age 70½, allowing more assets to grow in these tax-deferred accounts. Additionally, the rules for distributions were relaxed, allowing up to $5,000 in penalty-free distributions from an IRA to cover child birth or adoption expenses, and $10,000 in distributions from 529 plans to repay student loans. To partially pay for these beneficial provisions, the SECURE Act also requires inherited IRAs to now be distributed within 10 years from the nonspouse owner’s date of death, instead of a usually much longer period based on the beneficiary’s life expectancy.

The CARES Act contained a number of tax provisions benefitting individuals and a number of other provisions affecting tax reporting. Perhaps most predominantly, the CARES ACT included a recovery rebate of up to $1,200 ($2,400 for married couples) while also expanding the amount and availability of unemployment insurance. In addition, many people qualify to take up to $100,000 of early distributions from a retirement plan, without penalty, while spreading the resulting income over three years. Finally, the CARES Act waived the RMD requirement for 2020 for all taxpayers.

For businesses, the CARES Act featured provisions aimed at retaining employees and allowing deduction of losses. The aptly named employee retention credit allows a payroll tax credit for 50 percent of wages paid to employees for certain businesses whose business was fully or partially suspended, or whose gross receipts decreased by 50 percent for the quarter. In addition, employers could defer the payment of the employer portion of Social Security taxes. Perhaps most significantly, the CARES Act allows net operating losses from 2018, 2019 and 2020 to be carried back up to five years, which could create valuable refund opportunities for businesses looking to increase their immediate cash flow.

With the effects of the pandemic now increasing again on a daily basis, the impact of these new tax provisions that have become effective in 2020 should be considered now in order to ensure that you take advantage of any tax savings opportunities available. This year, tax savings for individuals and small businesses may be more crucial than ever as the country tries to get back on track. Furthermore, the new approach of “timing” taxable income and deductions rather than broadly deferring income and accelerating deductions may create additional tax saving opportunities over a two-year timeline.

This guide provides tax planning strategies for corporate executives, businesses, individuals, nonprofit entities and trusts. We hope that this guide will help you leverage the tax benefits available to you presently, or reinforce the tax savings strategies you may already have in place, or develop a tax-efficient plan for 2020 and 2021 as tax changes materialize under new leadership in America.

For your convenience, below is a quick reference guide of action steps that can help you reach your tax-minimization goals, as long as you act before the clock strikes midnight on January 1, 2021. Not all of the action steps will apply in your particular situation, but you could likely benefit from many of them. Taxpayers may want to consult with us to develop and tailor a customized plan, with defined multiyear tax modeling to focus on the specific actions that you are considering as tax changes, perhaps favorable or unfavorable, undoubtedly loom. We will be pleased to help you analyze the options and decide on the strategies that are most effective for you, your family and your business.

Whether you should accelerate taxable income or defer deductions between 2020 and 2021 largely depends on your projected highest (aka marginal) tax rate for each year (with tax rates for 2020 clearly known and those for 2021 less certain). While the highest official marginal tax rate for 2020 is currently 37 percent, you might pay more tax than in 2019 even if you were in a higher tax bracket due to credit fluctuations, long term capital gains, qualified dividends or myriad other reasons.

The chart below summarizes the most common 2020 tax rates together with corresponding taxable income levels. Effective management of your tax bracket can provide meaningful tax savings, as often a change of $1 in taxable income can shift you into the next higher or lower bracket. These differences can be further exacerbated by other income thresholds throughout the code, and discussed in this guide, such as those for determining eligibility for the child tax credit and qualified business income deductions, among others. Income deferral and acceleration, while being mindful of bracket thresholds, can be accomplished through numerous income strategies discussed in this guide, such as retirement distribution planning, bonus acceleration or deferral and harvesting of capital gains and losses.

2020 Federal Income Tax Rate Schedule

|

Tax Rate |

Single |

Head of Household |

Married Couple |

|

10% |

$0 - $9,875 |

$0 - $14,100 |

$0 - $19,750 |

|

12% |

$9,876 - $40,125 |

$14,101 - $53,700 |

$19,751 - $80,250 |

|

22% |

$40,126 - $85,525 |

$53,701 - $85,500 |

$80,251 - $171,050 |

|

24% |

$85,526 - $163,300 |

$85,501 - $163,300 |

$171,051 - $326,600 |

|

32% |

$163,301 - $207,350 |

$163,301 - $207,350 |

$326,601 - $414,700 |

|

35% |

$207,351 - $518,400 |

$207,351 - $518,400 |

$414,701 - $622,050 |

|

37% |

Over $518,400 |

Over $518,400 |

Over $622,051 |

While reviewing this guide, please keep the following in mind:

- Never let the tax tail wag the financial dog, as we often preach. Always assess economic viability. This guide is intended to help you achieve your personal and business financial objectives in a “tax efficient” manner. It is important to note that proposed transactions should make economic sense in addition to saving on taxes. Therefore, you should review your entire financial position prior to implementing changes. Various nontax factors can influence your year‑end planning, including a change in employment, your spouse reentering or exiting the work force, the adoption or birth of a child, a death in the family or a change in your marital status. It is best to look at your tax situation for at least two years at a time with the objective of reducing your tax liability for both years combined, not just for 2020 in isolation… especially at this time in our lives. In particular, multiple years should be considered when implementing “bunching” or “timing” strategies, as discussed throughout this guide.

- As we mentioned earlier herein, even if you do not expect your income to increase in 2021, there is always the possibility of tax rate increases on the horizon, with a new administration likely taking over in January and the economic pressures on the budget related to the pandemic. Of course, that economic pressure can cut both ways―it is also politically difficult to raise taxes during a difficult economic period. Since there are always uncertainties in the stock market, economy and tax environments, even now, we recommend the prudent approach of planning now and revising those plans as the need arises. As we noted earlier, another planning window to execute tax strategies from early January until a formal bill is introduced/passed may exist.

- As has been and will be our theme throughout this guide, the threat of sweeping tax increases with a Biden victory and a Republican-controlled Senate effective January 1, 2021 seem unlikely. As a result, many important year-end planning considerations exist for taxpayers unconcerned with potential income, capital gain and dividend rate increases.

- However, it’s important to note that while unlikely it certainly remains possible for Democrats to win the Senate and swiftly pursue tax increases. Your year-end planning challenge this year is to consider the best course of action in advance of potential tax increases which will not be absolutely known until January or later. So, if you are holding appreciated assets and planning to dispose of these assets early next year, you could consider accelerating the sale into 2020 to protect against the risk of a tax increase if the downside of such accelerated timing is not too costly. However, be very cautious about such accelerated timing in ways that you lose too much value, including the time value of money. That is, any decision to save taxes by accelerating income must consider the possibility that this means paying taxes on the accelerated income earlier, which would require you to forego the use of money used to satisfy tax liabilities that could have been otherwise invested. Accordingly, the time value of money can make a bad decision worse or, hopefully, a good decision better. A delicate balance indeed.

- While the traditional strategies of deferring taxable income and accelerating deductible expenses are the focus of this guide, with exceptions, you can often achieve overall tax efficiency by reversing this technique. For example, waiting to pay deductible expenses such as mortgage interest until 2021 would defer the tax deduction to 2021. Or, waiting to pay state and local taxes (SALT) until 2021 if you have already paid SALT of $10,000 in 2020 could also be worthwhile not only because of potential rate increases, but also if the $10,000 SALT cap is modified or repealed. You should consider deferring deductions and accelerating income if you expect to be in a higher tax bracket next year, you have charitable contribution carryovers to absorb, your marital status will change next year, or your head‑of‑household or surviving spouse filing status ends this year. This analysis can be complex, and you should seek professional guidance before implementation.

- Both individuals and business have many ways to “time” income and deductions, whether by acceleration or deferral. Businesses, for example, can make different types of elections that affect the timing of significant deductions. Faster or slower depreciation, including electing in or out of bonus depreciation for instance, is one of the most significant. This type of strategy should be considered carefully as it will not simply defer a deduction into the following year, but can push the deduction out much further or spread it over a number of years.

- Keep in mind―if you have analyzed your financial and tax situation, assessed the legislative outlook and determined that it still makes sense to act before year-end, there are a number of “timing” strategies available. Some changes may offer the flexibility of making a decision when filing the tax return for the year and do not need to be performed by year-end. At the end of the day, we recommend that you examine your tax situation now and consult with us.

With these words of caution in mind, following are observations and specific strategies that can be employed in the waning days of 2020 regarding income and deductions for the year, where the tried and true timing principles of deferring taxable income and accelerating deductible expenses will result in maximum tax savings.

Below is a quick and easy reference guide of action steps that can help you reach your tax-minimization goals, as long as you act before the clock strikes midnight on January 1, 2021. Not all of the action steps will apply in your particular situation, but you could likely benefit from many of them. In addition, several steps can be taken before year-end which are not necessarily “quick and easy,” but which could yield even greater benefits, such as setting up a private foundation to achieve your charitable goals (See item 89) and reviewing your estate plan and wealth transfer vehicles to utilize the current unified credit. (See items 92-100.) Consultation with us to develop and tailor a customized plan and to focus on the specific actions that should be taken is paramount, especially as tax changes to a certain degree are expected.

10 Income and Loss Quick-Strike Strategies

- Invest in a Qualified Opportunity Zone before year-end to defer and exclude gains (See item 10.)

- Coordinate timing of your capital gains and losses to minimize tax on your gains and maximize the tax benefit from your losses. (See item 23.)

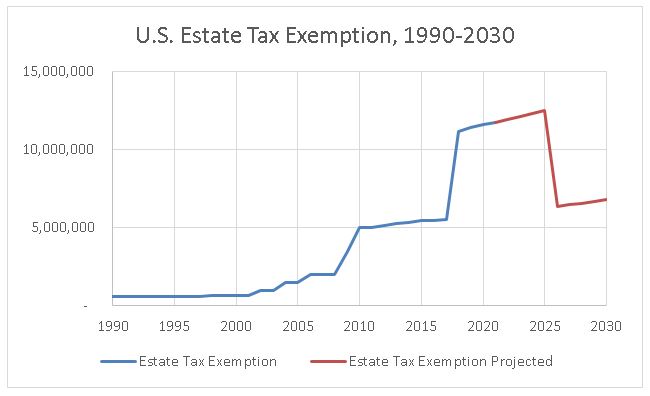

- As you sell securities at year end and harvest losses, ensure you do not run afoul of the wash-sale rule. (See item 26.)

- Make charitable gifts directly from your IRA, if you are age 70½ or older. (See item 44.)

- Increase your tax basis in pass-through entities so that you can deduct current year losses. (See item 49.)

- Defer loan modifications and the cancellation of debt until 2021. (See item 53.)

- Plan for worthless stock and substantiate the loss before year end. (See item 30.)

- Take advantage of new net operating loss (NOL) carryback rules under the CARES Act to inject much needed cash into your business. (See item 7.)

- Carefully plan Roth conversions. (See item 42.)

- Consider disposing of a passive activity to allow you to deduct suspended losses. (See item 48.)

10 Deduction and Credit Quick-Strike Strategies

- Claim all available employer credits under the CARES Act. (See item 1.)

- Time your purchases of business property and consider amending 2018 and 2019 returns to reclassify qualified improvement property (See item 67).

- Amend your 2019 return now to realize 2020 casualty losses from COVID. (See item 15.)

- Ensure that you are maximizing your retirement savings contributions in 2020 to reduce income in the current year and to achieve tax-deferred growth. (See item 39.)

- Defer payment of state and local taxes (income, sales and property) where possible if these payments already exceed $10,000 in 2020. (See item 18.)

- Prepay as many medical expenses in 2020 as possible if your unreimbursed medical expenses are close to exceeding 7.5 percent of adjusted gross income (AGI) for 2020. (See item 17.)

- Maximize your Qualified Business Income Deduction on pass-through income. (See item 62.)

- Consider purchasing qualified business property to take advantage of the $1 million business property expensing option. (See item 67.)

- Take advantage of expanded business interest limitation for 2020. (See item 6.)

- Apply a bunching strategy to itemized deductions such as medical expenses, charitable contributions and mortgage interest. (See item 46.)

1. Maximize new and expiring employer credits. With the passage of the CARES Act in March, Congress created multiple incentives for employers to hire and retain workers as they weathered the COVID-19 pandemic. First, the CARES Act created the employee retention credit, providing businesses with up to $5,000 of refundable credits per employee, based on 50 percent of the wages paid. In order to qualify, the business must not have received Paycheck Protection Program (PPP) loans and the wages must have been paid while the business was either suspended by government order or during a quarter in which receipts were down 50 percent over the prior year.

In addition, the CARES Act also allows employers to defer payment of the employer portion of social security taxes incurred between March 27 and December 31, 2020, into two equal payments due December 31, 2021, and December 31, 2022.

The Families First Coronavirus Response Act (FFCRA), enacted on March 18, 2020, created a new paid sick and family leave credit specifically to deal with COVID-19 infections and quarantines of employees as well as care for minors during school or childcare closures. While this credit is currently only available until December 31, 2020, it is entirely possible this credit will be extended as the pandemic drags on.

In addition, the family and medical leave credit created by the TCJA is also scheduled to expire on December 31, 2020. In order to qualify for this credit, employers' written policies must provide at least two weeks of paid leave for eligible full time employees and paid leave must be at least 50 percent of wages paid during a normal work week. The credit ranges for 12.5 percent to 25 percent of wages paid to qualified employees who are out for up to a maximum of 12 weeks during the year. Wages used to calculate the new paid leave credit under the FFCRA are not taken into account for purposes of calculating this credit.

Finally, the Work Opportunity Tax Credit is a nonrefundable credit for employers to take who employ certain individuals from targeted groups, such as veterans, low income individuals and ex-felons. The size of the credit depends on the hired person’s target group, the number of individuals hired and the wages paid to each. This credit is also scheduled to expire at the end of 2020.

2. Take advantage of changes to retirement contribution rules. Beginning in 2020 with the passage of the SECURE ACT, there is no longer an age limit for individuals who choose to contribute towards a traditional IRA. Previously, those who turned 70½ during the taxable year were ineligible to make any further contributions to their retirement account. Keep in mind that in order to contribute to a traditional IRA, a taxpayer needs to have earned income from a job or self-employment, so this only affects those seniors that are continuing to work after age 70½. The contribution limit for IRAs remains the same at $6,000 ($7,000 for those aged 50 and over), and the deductibility of contributions may be limited based on income or your eligibility for an employer plan.

3. Consider utilizing early withdrawals and loans from retirement plans for a needed cash injection. While removing assets from retirement accounts before retirement is always a method of last resort, as you would be giving up compounding growth, there has never been a better time to raid these plans if you are desperate for cash now. The CARES Act has waived the early retirement withdrawal tax penalty of 10 percent for those individuals who qualify in 2020. In order to qualify for the waiver of the tax, the individual must have been directly impacted by COVID-19. This means that either the taxpayer or a member of his or her family must have been infected with COVID-19 or have experienced adverse financial consequences related to COVID-19. Individuals are eligible to take up to $100,000 worth of distributions from their retirement plans before December 31, 2020. The distributions may be included as income either ratably over a three year period or fully in the year in which the distributions were made.

You could also take out a loan from an employer-sponsored plan, if the plan provides that option. You would be required to make loan repayments on a monthly basis and be responsible for any interest and taxes associated with the loan. However, the CARES Act allowed employers to increase the maximum loan amount up to $100,000 for loans made between March 27 and September 22, 2020. Also, certain repayments were delayed for up to a year for loans outstanding on March 27, 2020.

4. Consider special Required Minimum Distribution rules for 2020. Previously, if you were age 70½ or older, you would have been subject to the minimum distribution rules with regard to your retirement plans. Under these rules, you must receive at least a certain amount each year from your retirement accounts based on life expectancy tables. You can always take out more than the required amount, but anything less is subject to a 50 percent penalty on the shortfall amount.

Now, under the SECURE Act, if you reach age 70½ in 2020 or later, your first distribution is required by April 1 of the year after you turn 72. Additionally, due to the passage of the CARES Act in March, RMDs are not required to be taken in 2020. For individuals who turned 70½ in 2019 and were required to take their first distribution by April 1, 2020, and who did not take the distribution in 2019, they may skip this RMD as well.

While normally we do not recommend deferring income into another tax year, here it may advantageous to do so as you will allow your investment to continue to grow, reserving more capital for your later years. A careful timing assessment is needed. “Crunching the numbers” for 2020 and 2021 will help you to determine the optimal timing of any distributions, whether required or not while considering tax rate increase risk.

5. Consider accelerating 2021 charitable pledges into 2020 whether by cash, credit card or donor-advised funds. Good news here for charitable giving: For 2020, the AGI limitation for cash contributions to public charities is raised from 60 percent to 100 percent thanks to the CARES Act, meaning that more current year contributions are available as a deduction in 2020. Contributions made to a donor-advised fund are still subject to the 60 percent of AGI limitation, but these contributions will allow you to receive a tax deduction in the year contributed while enabling you to retain control of the timing of disbursements to specific charities in a later period, at your direction. In addition, prior year carryovers remain subject to the 60 percent of AGI limitation.

Remember that regardless of form, charitable contributions of money must be supported by a canceled check, bank record or receipt from the donee organization showing the name of the organization, the date of the contribution and the amount of the contribution.

6. Be sure to receive maximum benefit for business interest. Under the TCJA, the interest expense deduction was limited to 30 percent of the adjusted taxable income of the business, applicable at the entity level for partnerships and S corporations. Certain smaller businesses (less than an inflation indexed $25 million in average annual gross receipts for the three-year tax period ending with the prior tax period) were exempt from this limitation. In addition, real property trades or businesses can elect out of the limitation if they use the alternative depreciation system (ADS) to depreciate applicable real property used in a trade or business.

However, the CARES Act has changed the business interest limitation from the aforementioned 30 percent of adjusted taxable income to 50 percent for years 2019 and 2020. The switch from 30 percent to 50 percent could potentially increase available deductions and even create net operating losses (NOLs) for businesses during 2020. This could lead to potential tax savings and refund opportunities for businesses with debt or those with difficult circumstances due to the COVID-19 crisis.

A few things should be kept in mind in terms of the effect the CARES Act had on business interest. While the increase from 30 percent to 50 percent generally applies to tax years 2019 and 2020, this increase to 50 percent does not apply to partnerships in 2019, only for 2020, while also allowing deduction of 50 percent of the 2019 excess business interest expense carryforward without regard to the limitation.

Taxpayers that have already filed 2019 tax returns can amend to change from 30 percent to 50 percent in order to secure refunds (with the exception of partnerships).

7. Consider carrying back NOLs to generate immediate cash. One of the provisions contained in the CARES Act earlier this year greatly expanded opportunities with respect to NOL planning. Previously, under the TCJA, NOLs were permitted to be carried forward but not back to prior years. In addition, the deductible amount was limited to 80 percent of a taxpayer’s taxable income.

Now, under the CARES Act, the 80 percent income limitation for NOL deductions for years 2018, 2019 and 2020 are suspended indefinitely. Furthermore, losses arising in 2019 and 2020 may be carried back and used to offset prior year income for the preceding five years. (Unfortunately, the window for taxpayers to recognize an NOL during 2018 and file for a carryback adjustment claim expired in June of 2020, though the window remains open for 2019.)

The modifications under the CARES Act with respect to NOLs could boast potential significant refund opportunities. For instance, if you did not incur any business losses before the pandemic and now sustain losses in 2020, you may carryback your 2020 NOL to previous profitable years in order to secure a refund of previously paid income taxes.

Businesses that are being affected by COVID-19 and expect losses into 2021 and beyond will not be able to carry back losses under the CARES Act. Therefore, taxpayers should consider other tactics such as accelerating expenses in the current year to the extent of income over the past five years. An example would be the purchasing of depreciable assets and electing bonus depreciation in 2020 with the intent to decrease current-year income while increasing the NOL carryback.

It is important to keep in mind that carrying back a loss could have adverse effects on other items of a tax return. Please analyze the scenarios and discuss with a trusted tax adviser before making any decisions.

8. Lease modifications may generate unintended tax consequences. IRC Section 467 was originally enacted as an anti-abuse provision to prevent tax shelters that took advantage of certain timing differences. Section 467 can result in the inclusion of income if lease terms are substantially modified by:

- Increasing/decreasing the lease payments;

- Shortening/extending the lease term; and/or

- Deferring/accelerating lease payments due.

Moving forward, lease modifications will remain a very complicated issue. Comprehensive contract analysis and Section 467 testing will be required on a case by case basis as lessors and lessees continue to navigate the COVID-19 crisis.

9. Be mindful of PPP forgiveness concerns. Congress created the Paycheck Protection Program, better known as “PPP,” back in March 2020 as the COVID-19 pandemic continued to ravage the U.S. economy, forcing thousands of businesses to abruptly shutter (We previously wrote about PPP forgiveness in this Alert). The PPP was included in the $2 trillion CARES Act in order to authorize the funding of forgivable loans of up to $10 million per borrower, which qualifying businesses could spend to cover payroll, mortgage interest, rent and utilities expenses.

Loans were made available to small businesses with 500 or fewer employees for an array of business industries including: not-for-profits, self-employed individuals, sole proprietorships, veterans’ organizations and independent contractors. In addition, businesses with more than 500 employees in certain industries were also able to apply for loans. Congress intended to give support to organizations facing economic instability due to the ongoing COVID-19 pandemic, most notably to provide assistance so employees could continue to earn their salaries. As such, PPP loan forgiveness is largely based on maintaining prepandemic employees and salaries.

Since being enacted in March, the PPP program was substantially modified by the PPP Flexibility Act in June (which we wrote about in this Alert), and various additional guidance from the Small Business Administration. As the pandemic worsens again and new lockdowns loom, taxpayers around the country await additional aid, modifications and relaxation of the PPP rules.

While acceptance of some loan forgiveness applications began in August, most borrowers should hold off on submitting their loan forgiveness application. Like many other topics under the CARES Act, with guidance continuing to evolve, taxpayers should consult with trusted tax advisers before making any decisions.

10. Invest in Qualified Opportunity Zones to save on capital gains. Gains can be deferred on the sale of appreciated stock that is reinvested within 180 days into a Qualified Opportunity Fund (QOF). For 2020, special rules are in place allowing taxpayer to invest eligible gain into a QOF by December 31, 2020, if their 180-day period would have ended between April 1 and December 31, 2020. So if you have some gains from earlier in the year and look to be in a gain position for the year, you now have an extension to get that gain into a QOF, as long as you act before the end of the year.

If the investment is held for over 10 years, the gain after acquisition can be entirely eliminated. The investment can be in the form of an investment interest in either a partnership or corporation that invests 90 percent of its assets in a Qualified Opportunity Zone. All states have qualified communities that now qualify. Besides investing in a fund, one can also take advantage of this opportunity by establishing a business in the Qualified Opportunity Zone or by investing in Qualified Opportunity Zone property.

11. Claim a refund of the Corporate Alternative Minimum Tax (AMT) Credit. For 2018, the corporate AMT was repealed by the TCJA. However, corporations that paid AMT in 2017 and earlier were allowed to carry forward AMT paid as a credit against regular tax. With the passage of the CARES Act in March, now corporate taxpayers can claim 100 percent of any remaining credit, regardless of tax liability, beginning in 2019. Alternatively, taxpayers could also elect to claim the refundable credit in 2018 (on an amended return) for an immediate cash infusion. If your business still has AMT credits remaining, please contact us so we can prepare the necessary filings to get your business cash now.

12. Enjoy increased charitable contribution limits for C corporations. Normally, corporations are limited to charitable contributions of 10 percent of taxable income. However, with the passage of the CARES Act, this limit is increased to 25 percent of taxable income for the 2020 year only. Also, while the deduction for contribution of food inventory is usually limited to 15 percent of net income, this has been raised to 25 percent for 2020 only. This limit will allow more grocery and package stores to donate to local food banks and shelters to combat the food insecurity plaguing parts of the country.

13. File protective claims to ensure eligibility for tax refunds related to the Affordable Care Act (ACA). As was heavily publicized relating to the confirmation of Supreme Court Justice Amy Coney Barrett, the U.S. Supreme Court recently heard a case on the ACA, in which it may decide the constitutionality of the law as whole, including certain taxes paid under the act, such as the 3.8 percent Net Investment Income Tax (NIIT), the 0.9 percent Additional Medicare Tax and the individual mandate penalty (repealed for tax years beginning after December 31, 2018). Should the entire law be declared unconstitutional, taxpayers may be eligible for refunds of these taxes, subject to the statute of limitations on claims for refund.

Certain taxpayers prepared “protective claims” with the IRS that, should the law change, would preserve their right to claim a refund for 2016 before the statute of limitations expired on July 15, 2020 (Which we previously wrote about in this Alert). The statute of limitations for the 2017 tax year remains open, but for most taxpayers will expire on April 15, 2021. Contact us if you would to “crunch the numbers” and determine whether a protective claim may benefit you.

14. Complete a solar installation prior to year-end for maximum benefit. Currently, the Solar Investment Tax Credit (ITC) allow for a credit of 26 percent of eligible expenses for projects commenced in 2020. For projects commenced in 2021, this credit will drop to 22 percent of eligible expenses, though legislation is currently being considered which may extend the 26 percent credit (or prior 30 percent credit).

15. Take advantage of casualty and disaster losses from COVID. Due to the ongoing COVID-19 pandemic, President Trump declared an “emergency” under the Stafford Act in March 2020, subsequently approving all major disaster requests for all 50 states, D.C. and other various U.S. territories. This “disaster declaration,” as it is commonly known, was unprecedented in scope. As a direct result, under IRS regulations (specifically IRC Sec. 165(i)), any loss occurring in a federally deemed disaster zone may, at the election of the taxpayer, be considered for the taxable year immediately preceding the taxable year in which the disaster occurred.

Thus, any losses that were considered attributable to COVID-19 after March 13, 2020, could be pushed back into 2019, such as the closure of stores, losses on mark-to-market securities and permanent retirement of fixed assets. However, lost revenues and the decline in fair market value of property as a direct result of COVID-19 economic hardships would not constitute a loss under IRC. Sec 165(i).

While we are beyond the point where taxpayers could include the loss on their 2019 tax return (the due date was October 15, 2020), it is still possible for taxpayers to go back and amend 2019 filings, especially if 2019 profits could be offset with 2020 disaster losses. The subject of COVID-19 disaster losses remains a very complicated matter, and there are many rules and stipulations that would prevent taxpayers from taking advantage of the election. There are also certain reasons why taxpayers would not want to make the election. For those reasons, we recommend that you consult with us before delving into the amending process.

16. Review the increased standard deduction. For 2020, the standard deduction has increased slightly to $24,800 for a joint return and $12,400 for a single return. Taxpayers age 65 or older and those with certain disabilities may claim increased standard deductions.

|

Standard Deduction (Based on Filing Status) |

2019 |

2020 |

|

Married Filing Jointly |

$24,400 |

$24,800 |

|

Head of Household |

$18,350 |

$18,650 |

|

Single (Including Married Filing Separately) |

$12,200 |

$12,400 |

17. Pay any medical bills in 2020. The medical expense deduction floor remains at 7.5 percent of AGI for 2020. In addition, the deduction is no longer an AMT preference item, meaning that even taxpayers subject to the AMT would benefit from deductible medical expenses. However, this deduction is currently scheduled to revert to a 10 percent floor and being an AMT preference item in 2021, barring congressional action. While this is a politically popular deduction on both sides of the aisle and Congress may elect to extend the lower deduction floor to 2021, it has not yet been extended.

18. Defer your state and local tax payments into 2021. One of the most notable changes enacted by the TCJA in 2017 was the limitation of the state and local tax deduction. In 2020, the deduction limit for state and local income or sales and property taxes of $10,000 per return ($5,000 in the case of a married individual filing separately) remains unchanged.

19. Prepay your January mortgage payment if you will be under the mortgage interest limitation. For acquisition indebtedness incurred after December 15, 2017, the mortgage interest deduction is limited to interest incurred on up to $750,000 of debt ($375,000 in the case of a married individual filing a separate return). The mortgage interest from both a taxpayer’s primary and secondary residences remains deductible, up to this balance limit on newer debt. Home equity indebtedness not used to substantially improve a qualified home is no longer deductible. Debt existing prior to December 15, 2017, remains limited to the prior law amount of $1 million for original mortgage debt.

20. Take advantage of the child tax credit. The child tax credit will remain at $2,000 for 2020 for each qualifying dependent child age 16 or younger at the end of the tax year. The child tax credit is phased out beginning at $400,000 of modified adjusted gross income for joint filers ($200,000 for all other filers). In addition, the child tax credit is refundable to lower income taxpayers without an income tax liability, up to $1,400. Finally, nonqualifying child dependents (such as dependents over the age of 16, or those that do not meet the relationship test of a qualifying child) also qualify taxpayers for a $500 nonrefundable child tax credit per dependent.

Tax-Efficient Investment Strategies

For 2020, the long-term capital gains and qualifying dividend income tax rates, ranging from zero to 20 percent, have increased incrementally, as indicated in the table below.

|

Long-Term Capital Gains Rate |

Single |

Married Filing Jointly |

Head of Household |

Married Filing Separately |

|

0% |

Up to $40,000 |

Up to $80,000 |

Up to $53,600 |

Up to $40,000 |

|

15% |

$40,001 -$441,450 |

$80,001 -$496,600 |

$53,601 -$469,050 |

$40,001 -$248,300 |

|

20% |

Over $441,450 |

Over $496,600 |

Over $469,050 |

Over $248,300 |

In addition, a 3.8 percent tax on net investment income applies to taxpayers with modified adjusted gross income (MAGI) that exceeds $250,000 for joint returns ($200,000 for singles). Here are some ways to capitalize on the lower rates as well as other tax planning strategies for investors.

21. Maximize preferential capital gains tax rates. In order to qualify for the lower 20, 15 or zero percent capital gain rate, a capital asset must be held for at least one year. That is why it is important when disposing of your appreciated stocks, bonds, investment real estate and other capital assets to pay close attention to the holding period. If it is less than one year, consider deferring the sale so you can meet the longer-than-one-year period (unless you have short-term losses to offset the potential gain). While it is generally not wise to let tax implications be your only consideration in making investment decisions, you should not ignore them either. Keep in mind that realized capital gains may increase AGI, which in turn may reduce your AMT exemption and therefore increase your AMT exposure, although to a much lesser extent than in years past, given the increased AMT exemptions.

22. Reduce the recognized gain or increase the recognized loss. When selling stock or mutual fund shares, the general rule is that the shares you acquired first are the ones deemed sold first. However, if you choose, you can specifically identify the shares you are selling when you sell less than your entire holding of a stock or mutual fund. By notifying your broker of the shares you want sold at the time of the sale, your gain or loss from the sale is based on the identified shares. This sales strategy gives you better control over the amount of your gain or loss and whether it is long-term or short-term. One downfall of the specific identification method is that you may not use a different method (e.g., average cost method or first in, first out method) to identify shares of that particular security in the future. Rather, you will have to specifically identify shares of that particular security throughout the life of the investment, unless you obtain permission from the IRS.

23. Harvest your capital losses. It always makes sense to periodically review your investment portfolio to see if there are any “losers” you should sell. This year, with the ongoing volatility in the stock market, there are likely capital losses lurking somewhere in your portfolio. As year-end approaches, so does your last chance to offset capital gains recognized during the year or to take advantage of the $3,000 ($1,500 for married separate filers) limit on deductible net capital losses. However, one must be mindful not to run afoul of the wash-sale rule, discussed at item 26.

24. Take advantage of Section 1202 small business stock gain exclusion. For taxpayers other than corporations, Section 1202 allows for the potential exclusion of up to 100 percent of the gain recognized on the sale of qualified small business stock (QSBS) that is held more than five years, depending upon when the QSBS was acquired. The gain eligible for exclusion cannot exceed the greater of $10 million, or 10 times the aggregate adjusted basis of QSBS stock disposed of during the year. As an alternative, if the stock is held for more than six months and sold for a gain, you can elect to roll over and defer the gain to the extent that new QSBS stock is acquired during a 60-day period beginning on the date of the sale.

25. Be mindful of change in “kiddie tax” rules. Under the TCJA, for 2018 and 2019 the investment income of a child was taxed independently of the parents’ rates, utilizing the compressed tax brackets applicable to trusts and estates. The passage of the SECURE Act last year reset these rules back to 2019 law and reverted to the old set of rules for 2020. For 2020 and later tax years, the unearned income of children subject to the kiddie tax in excess of $2,200 are generally taxed at the parent’s tax rate.

For kiddie tax purposes, a child is defined as someone that has not yet reached the age of 18 by the end of the year, or an 18 year old or a full-time student aged 19-23 who does not support him or herself.

- Owners of Series EE and Series I bonds may defer reporting any interest (i.e., the bond’s increase in value) until the year of final maturity, redemption or other disposition. (If held in the parent’s name and used for qualified higher education expenses, and assuming certain AGI requirements are met, the income is not taxed at all.)

- Municipal bonds produce tax-free income (although the interest on some specialized types of bonds may be subject to the AMT).

- Growth stocks that pay little dividends and focus more on capital appreciation should be considered. The child could sell them after turning 23 and possibly benefit from being in a low tax bracket. Selling them before then could convert a potential zero percent income tax on the gain into a 20 percent income tax.

- Funds can be invested in mutual funds that concentrate on growth stocks and municipal bonds that limit current income and taxes. They may also limit risk through investment diversification.

- Unimproved real estate that will appreciate over time and does not produce current income will limit the impact of the kiddie tax.

- 529 plans offer investors the opportunity to experience tax-free growth, so long as distributions are used to fund qualified education expenses, discussed later at item 34. In addition, contributions to a 529 plan may qualify the donor for a deduction on his or her state income tax return.

26. Keep the wash-sale rules in mind. Often overlooked, the wash-sale rule provides that no deduction is allowed for a loss if you acquire substantially identical securities within a 61‑day period beginning 30 days before the sale and ending 30 days after the sale. Instead, the disallowed loss is added to the cost basis of the new stock. However, there are ways to avoid this rule. For example, you could sell securities at a loss and use the proceeds to acquire similar, but not substantially identical, investments. If you wish to preserve an investment position and realize a tax loss, consider the following options:

- Sell the loss securities and then purchase the same securities no sooner than 31 days later. The risk inherent in this strategy is that any appreciation in the stock that occurs during the waiting period will not benefit you.

- Sell the loss securities and reinvest the proceeds in shares of a mutual fund that invests in securities similar to the one you sold or reinvest the proceeds in the stock of another company in the same industry. This approach considers an industry as a whole, rather than a particular stock. After 30 days, you may wish to repurchase the original holding. This method may reduce the risk of missing out on any anticipated appreciation during the waiting period.

- Buy more of the same security (double up), wait 31 days and then sell the original lot, thereby recognizing the loss. This strategy allows you to maintain your position but also increases your downside risk. Keep in mind that the wash-sale rule typically will not apply to sales of debt securities (such as bonds) since such securities usually are not considered substantially identical due to different issue dates, rates of interest paid and other terms.

27. Lower your tax burden with qualified dividends. The favorable capital gain tax rates (20, 15 or zero percent) make dividend-paying stocks as attractive as ever, since their preferential lower rates will likely be preserved if the Senate remains in Republican control. This may cause you to reconsider the makeup of your investment portfolio. Keep in mind that to qualify for the lower tax rate on dividends the shareholder must own the dividend-paying stock for more than 60 days during the 121-day period beginning 60 days before the stock’s ex-dividend date. For certain preferred stock, this period is expanded to 90 days during a 181-day period.

28. Consider tax-exempt opportunities from municipal bonds, municipal bond mutual funds or municipal ETFs. Tax‑exempt interest is not included in adjusted gross income, so deduction items based on AGI are not adversely affected. As long as your investment portfolio is appropriately diversified, greater weight in municipal bonds may be advantageous. However, be mindful of the AMT impact on income from private activity bonds, which is still a preference item for AMT purposes. In general, a private activity bond is a municipal bond issued after August 7, 1986, whose proceeds are used for a private (i.e., nonpublic) purpose. Accordingly, review the prospectus of the municipal bond fund to determine if it invests in private activity bonds. Anyone subject to the AMT, including those with incentive stock options, should avoid these funds.

29. Time your mutual fund investments. Before you invest in a mutual fund prior to February 2021, you should contact the fund manager to determine if dividend payouts attributable to 2020 are expected. If such payouts take place, you may be taxed in 2020 on part of your investment. You need to avoid such payouts, especially if they include large capital gain distributions. In addition, certain dividends from mutual funds are not “qualified” dividend income and therefore are subject to tax at the taxpayer’s marginal income tax rate, rather than at the preferential 20, 15 percent (or zero percent) rate.

30. Determine worthless stock in your portfolio. Your basis in stock that becomes worthless is deductible (generally as a capital loss) in the year it becomes worthless, but you may need a professional appraiser’s report or other evidence to prove the stock has no value. Instead, consider selling the stock to an unrelated person for at least $1, or writing a letter to the officers of the company, abandoning the stock. You have now eliminated the need for an appraiser’s report and are almost guaranteed a loss deduction.

31. Consider the greatest tax exclusion hidden in your home. Federal law (and many, but not all, states) provides that an individual may exclude, every two years, up to $250,000 ($500,000 for married couples filing jointly) of gain realized from the sale of a principal residence. The exclusion ordinarily does not apply to a vacation home. However, with careful planning, you may be able to apply the exclusion to both of your homes.

32. Consider like-kind exchanges. A like-kind exchange provides a wonderful alternative to selling property outright. The traditional sale of property may cause you to recognize and pay taxes on any gain on the sale. A like-kind exchange, on the other hand, allows you to avoid gain recognition through the exchange of qualifying like-kind properties. The gain on the exchange of like-kind property is effectively deferred until you sell or otherwise dispose of the property you receive in the exchange. Beginning in 2018, like-kind exchanges are only available for real property sales. Also, while Democratic control of the Senate is unclear at this time, it should be noted that President-elect Biden did propose doing away with like-kind exchange gain.

- You wish to avoid recognizing taxable gain on the sale of property that you will replace with like-kind property;

- You wish to diversify your real estate portfolio without tax consequence by acquiring different types of properties with the exchange proceeds;

- You wish to participate in a very useful estate planning technique (continued like-kind exchanges allow you to permanently avoid recognition of gain); or

- You would generate an alternative minimum tax liability upon recognition of a large capital gain in a situation where the gain would not otherwise be taxed. (The like-kind exchange shelters other income from the alternative minimum tax.)

However, President-elect Biden has proposed eliminating the preferential rate for long-term capital gains and qualified dividends on income over $1 milllion, resulting in a potential capital gain tax rate increase from 20 percent to 39.6 percent. So, a like-kind exchange may not make sense if you expect to ultimately sell the replacement property while in the 39.6 percent tax rate.

33. Understand the tax implication of any cryptocurrency transactions. While most cryptocurrency exchanges are not required to issue formal tax documentation to traders, the IRS has already been requesting records from major exchanges and is cracking down on this industry as a whole. Gains and losses from the sale of cryptocurrencies, just like the sale of stock, are required to be reported on your tax return. As taxpayers are generally not provided with tax documents detailing sale prices and cost basis, taxpayers must track these items themselves to accurately report their income. Proper recording of basis in cryptocurrency can significantly decrease the capital gains, which may be assessed in the future should the IRS start requesting sales information from more exchanges.

Planning for Higher Education Costs

Many tax savings opportunities exist for education-related expenses. If you or members of your family are incurring these types of expenses now or will be in the near future, it is worth examining them in some detail. Here, in abbreviated form, are some strategies to consider as year-end approaches.

34. Plan ahead for tax-free growth with 529 qualified tuition plans. One of the best features of 529 plans is that the ownership and control of the plan lies with the donor (typically the parent or grandparent of the beneficiary student) and not with the beneficiary, so the plan is not considered an asset of the student for financial aid purposes, generally resulting in higher financial aid. For federal income tax purposes, plan contributions are on an after-tax basis, although many states allow a deduction. Contributions and earnings on contributions that are subsequently distributed for qualified higher education expenses (including tuition, room and board, and other expenses) at accredited schools anywhere in the United States are free of federal income tax and may be free of state income tax. Since 2018, 529 plan owners can use tax-free distributions for up to $10,000 of eligible expenses at elementary and secondary schools, in addition to colleges and universities. Since the SECURE Act was passed last December, tax-free distributions can be used to pay for eligible expenses related to an apprenticeship program, in addition to higher education expenses. The SECURE ACT also allows up to $10,000 of distributions to pay principal or interest on a qualified education loan of the beneficiary or a sibling of the beneficiary.

To the extent that distributions are not for qualified higher education expenses, regular income tax plus a 10 percent penalty may apply to the earnings portion of the distribution. As contrasted with the other education strategies discussed below, contributions may be made regardless of the donor’s AGI.

An election can also be made to treat a contribution to a Section 529 plan as having been made over a five-year period; consequently, for 2020 a married couple can make a $150,000 contribution to a Section 529 plan without incurring any gift tax liability or utilizing any of their unified credit, since the annual gift exclusion for 2020 is $15,000 per donor and the contribution can be split with the donor’s spouse. It is important to note that additional gifts made in the five-year period to the same donees have a high chance of triggering a gift tax filing obligation.

35. Take advantage of education credit options. If you pay college or vocational school tuition and fees for yourself, your spouse or your children, you may be eligible for either the American Opportunity Tax Credit (AOTC) or the Lifetime Learning Credit. These credits reduce taxes dollar-for-dollar, but begin to phase out when 2020 AGI exceeds certain levels. The chart below provides a summary of the phaseouts.

|

2020 Education Expense and Credit Summary |

|||

|

Tax Benefit |

Single filers (not including Married Filing Separately) |

Joint filers |

Maximum credit/ deduction/contribution |

|

American Opportunity Tax Credit |

$80,000 - $90,000 |

$160,000 - $180,000 |

$2,500 (credit) |

|

Lifetime Learning Credit |

$59,000 - $69,000 |

$118,000 - $138,000 |

$2,000 (credit) |

|

Student loan interest deduction |

$70,000 - $85,000 |

$140,000 - $170,000 |

$2,500 (deduction) |

|

Coverdell Education Savings Account |

$95,000 - $110,000 |

$190,000 - $220,000 |

$2,000 (contribution)

|

36. Remit additional student loan payments. The CARES Act gave temporary payment relief to borrowers of certain qualifying federal student loans. If your federal loans qualified, the U.S. Department of Education has automatically placed your loans in “administrative forbearance” through December 31, 2020. During this time, you are not required to make any payments and your applicable interest rate was adjusted to zero percent. You should consider making a payment by December 31, 2020, which will go directly towards your principal and may help you reduce your balance owed faster.

If your loan did not qualify for administrative forbearance or if you paid interest with respect to the period of January 2020 through March 2020 on a qualifying federal student loan, an “above the line” deduction of up to $2,500 is allowed for interest due and paid in 2020. Note the deduction is disallowed for taxpayers electing the filing status of married filing separate. The deduction is phased out when AGI exceeds certain levels. See chart above.

37. Contribute to a Coverdell Education Savings Account. These accounts must be established in a tax-exempt trust or custodial account organized exclusively in the United States. At the time the trust or account is established, the designated beneficiary must be under 18 (or a special needs beneficiary), and all contributions must be made in cash and are not deductible. The maximum annual contribution is limited to $2,000 per year, and the contribution is phased out when AGI exceeds certain levels. Distributions from Coverdell Education Savings Accounts are excludable from gross income to the extent that the distributions do not exceed the qualified education expenses incurred by the designated beneficiary, which include kindergarten through grade 12 and higher education expenses. If distributions exceed qualified expenses, a portion of the distributions is taxable income to the designated beneficiary. Furthermore, to the extent that distributions are not used for educational expenses, a 10 percent penalty applies.

Strategies to Implement Throughout the Year

Virtually any cash-basis taxpayer can benefit from and exercise a fair amount of control over strategies that accelerate deductions or defer income based on the premise that it is generally better to pay taxes later rather than sooner (especially when income tax rates are not scheduled to increase). For example, a check you deliver or mail during 2020 generally qualifies as a payment in 2020, even if the check is not cashed or charged against your account until 2021. Similarly, payments of deductible expenses by credit cards are not deductible when you pay the credit card bill (for instance, in 2021), but when the charge is made (for instance, in 2020).

With respect to income deferral, cash-basis businesses, for example, can delay year-end billings so that they fall in the following year or accelerate business expenditures to the current year. On the investment side, income from short-term (i.e., maturity of one year or less) obligations like Treasury bills and short-term certificates of deposit is not recognized until maturity, so purchases of such investments at this time will push taxability of such income into 2021. For a wage earner (excluding an employee-shareholder of an S corporation with a 50 percent or greater ownership interest) who is fortunate enough to be expecting a bonus, he or she may be able to arrange with his or her employer to defer the bonus (and his or her tax liability for it) until 2021. However, if any of this income becomes available to the wage earner, whether or not cash is actually received, the bonus will be taxable in 2020. This is known as the constructive receipt doctrine.

38. Help a disabled loved one maintain a healthy, independent and quality lifestyle with an ABLE account. An ABLE account is a tax-advantaged savings vehicle which can be established for a designated beneficiary who is disabled or blind. Only one account is allowed per beneficiary, though any person may contribute to an ABLE account. Contributions to an ABLE account are not deductible, but the earnings in the account grow on a tax-deferred basis and may be distributed tax free if used for qualified disability expenses, including basic living expenses such as housing, transportation and education, as well as medical necessities. If distributions are used for nonqualified expenses, the portion of the distribution that represents earnings on the account is subject to income tax plus a 10 percent penalty tax.

Total annual contributions by all persons to the ABLE account cannot exceed the gift tax exclusion amount ($15,000 for 2019 and 2020), though additional annual contributions may be possible if the beneficiary is employed or self-employed. States have also set limits for allowable ABLE account savings. If you are considering an ABLE account, contact us for further information.

39. Participate in and maximize payments to 401(k) plans, 403(b) plans, SEP (self‑employed) plans, IRAs, etc. These plans enable you to convert a portion of taxable salary or self‑employed earnings into tax deductible contributions to the plan. In addition to being deductible themselves, these items increase the value of other deductions since they reduce AGI. Deductible contributions to IRAs are generally limited to $6,000 in 2020, while substantially higher amounts can be contributed to 401(k) plans, 403(b) plans and simplified employee pensions (SEPs). For 2020, the deduction for IRA contributions starts being phased out if you are covered by a retirement plan at work and your AGI exceeds $65,000 for single filers and $104,000 for married joint filers. In 2020, $19,500 may be contributed to a 401(k) plan as part of the regular limit of $57,000 that may be contributed to a defined contribution (e.g., money purchase, profit‑sharing) plan. These limits have both increased in 2020 and are reflected in the table below. Don’t forget that additional catch-up contributions are allowed for those taxpayers ages 50 and above, as noted in the chart below.

In addition, SEPs can be established and contributed to as late as the due date of your return, including extensions, or as late as October 15, 2021, for tax year 2020.

|

Annual Retirement Plan Contribution Limits |

||

|

Type of Plan |

2019 |

2020 |

|

Traditional and Roth IRAs Catch-up contributions (ages 50+) for traditional and Roth IRAs |

$6,000 $1,000 |

$6,000 $1,000 |

|

Roth and traditional 401(k), 403(b) and 457 plans Catch-up contributions (ages 50+) for 401(k), 403(b) and 457 plans |

$19,000

$ 6,000 |

$19,500

$6,500 |

|

Simple Plans Catch-up contributions (ages 50+) for Simple Plans |

$13,000 $3,000 |

$13,500 $3,000 |

|

SEPs and defined contribution plans* |

$56,000 |

$57,000 |

* Annual limits for compensation must be taken into account for each employee in determining contributions or benefits under a qualified retirement plan. For 2020, the limit as adjusted for inflation is $285,000.

40. Participate in health and dependent care flexible spending accounts (IRC Section 125 accounts). These plans enable employees to set aside funds on a pretax basis for (1) medical expenses that are not covered by insurance up to $2,750 per year, (2) dependent‑care costs up to $5,000 per year ($2,500 for married persons filing separately) and (3) adoption assistance of up to $14,300 per year. Funds contributed by employees are free of federal income tax (at a maximum rate of 37 percent), Social Security and Medicare taxes (at 7.65 percent) and most state income taxes (at maximum rates as high as 11 percent), resulting in a tax savings of as much as 55.65 percent. Paying for these expenses with after‑tax dollars, even if they meet various AGI requirements, is more costly under the current tax rate structure. Since many restrictions apply, such as the “use it or lose it” rule, review this arrangement before making the election to participate.

For example, if John’s salary is $150,000 and Mary’s salary is $50,000, FSA contributions of $5,000 by John will not reduce his Social Security tax (since, even reflecting the FSA contributions, his Social Security wages exceed $137,700), while FSA contributions of $5,000 by Mary will save her approximately $300 in Social Security tax.

41. Participate in Health Savings Accounts (IRC Section 223 accounts). Health Savings Accounts (HSAs) are another pretax medical savings vehicle that are currently highly favored in the marketplace by Congress. HSAs offer a tax-favorable way to set aside funds to meet future medical needs. The four key elements to an HSA include: (1) contributions you make to an HSA are deductible, within limits; (2) contributions your employer makes are not taxed to you; (3) earnings on the funds within the HSA are not taxed; and (4) distributions from the HSA to cover qualified medical expenses are not taxed.

To be eligible for an HSA, you must be covered by a “high deductible health plan.” You must also not be covered by a plan that (1) is not a high deductible health plan and (2) provides coverage for any benefit covered by your high deductible plan. For self-only coverage, the 2020 limit on deductible contributions is $3,550. For family coverage, the 2020 limit on deductible contributions is $7,100.

42. Carefully plan Roth conversions. Converting a traditional retirement account such as a 401(k) or individual retirement account (IRA) into a Roth 401(k) or IRA will create taxable income upon conversion and allow tax-free distributions in retirement. There are many good reasons (and a few bad ones) for converting a 401(k) or traditional IRA to a Roth IRA. Good reasons include:

- You have special and favorable tax attributes that need to be consumed such as charitable deduction carry-forwards, investment tax credits and NOLs, among others;

- You expect the converted amount to grow significantly and tax-free growth is desired;

- Your current marginal income tax rate is likely lower than at the time of distribution (retirement);

- You have sufficient cash outside the 401(k) or traditional IRA to pay the income tax due as a result of the conversion;

- The funds converted are not required for living expenses, or otherwise, for a long period;

- You expect your spouse to outlive you and will require the funds for living expenses; and

- You expect to owe estate tax.

If you decide to rollover or convert from a 401(k) or traditional IRA to a Roth 401(k) or IRA and you also expect your AGI and tax bracket to remain more or less constant, you should consider staggering the total amount you plan to shift over a period of years. For example, a taxpayer who plans to convert a total of $185,000 from a regular IRA to a Roth IRA should consider converting $37,000 per year for five years. This strategy may prevent the conversion from pushing a taxpayer into a higher tax bracket, since the conversion is fully taxable on the amount converted.

43. Avoid deduction limits for noncash charitable contributions. Gifts of appreciated stock allow a taxpayer to mitigate taxes on capital gains, though the deduction for capital gain property is limited to 30 percent of AGI.

For personal property, the charitable deduction for airplanes, boats and vehicles may not exceed the gross proceeds from their resale. Form 1098-C must be attached to tax returns claiming these types of noncash charitable contribution. Furthermore, donations of used clothing and household items, including furniture, electronics, linens, appliances and similar items, must be in “good” or better condition to be deductible. You should maintain a list of such contributions together with photos to establish the item’s condition. To the extent they are not in “good condition,” you will need to secure a written appraisal to deduct individual items valued at more than $500.

|

Noncash Contribution Substantiation Guide |

||||

|

Type of Donation |

Amount Donated |

|||

|

Less than $250 |

$250 to $500 |

$501 to $5,000 |