The United States plunged off the theoretical cliff New Year's Day, but the U.S. House of Representatives pulled us back by passing the U.S. Senate's version of the budget bill on New Year's Day, and lo and behold, we now have clarity on tax rates and tax provisions for 2013 and beyond. While vacationing with his family in Hawaii, President Obama's signature was put on the legislation officially known as the "American Taxpayer Relief Act of 2012" (the Act) on January 2, 2013, by an autopen signing machine in Washington. In the most simplest terms, the legislation:

- Averts the tax side of the fiscal cliff, but simply delays sequestration (the automatic spending cuts) side by two months;

- Raises income taxes on individuals with income over $400,000 a year and families with income over $450,000 by more than 13% from a maximum rate of 35% to 39.6%;

- Raises capital gains and qualified dividend taxes on individuals with income over these levels by 33% from 15% to 20% (Incidentally, the 28% and 25% tax rates for collectibles and Section 1250 gain, respectively, continue without change after 2012);

- Imposes a stiff marriage penalty on couples, as married couples filing jointly with combined incomes of $450,000 are subject to the 39.6% rate instead of double the single threshold, or $800,000;

- Maintains the lower Bush-era ordinary tax at a maximum rate of 35% and capital gains and qualified dividend tax at a maximum rate of 15% for those not reaching these same income levels. However, taxes will be effectively raised on individuals earning more than $250,000 a year and families making more than $300,000 by limiting the previously suspended Personal Exemption Phase-out (PEP) and the previously suspended limitation on itemized deductions;

- Raises taxes for all wage-earners (and those self-employed) by not extending the 2% Social Security tax reduction;

- Permanently patches the Alternative Minimum Tax (AMT) so that more than 30 million taxpayers avoid this secretive and steep tax;

- Permanently extended the child and dependent care credit;

- Permanently raises the maximum federal estate tax rate on estates valued at $5 million for individuals and $10 million for couples, indexed for inflation, from 35% to 40%, unifies the estate and gift tax and maintains "portability" between spouses; and

- Retains many favorable tax breaks that were scheduled to expire, including but not limited to, tax-free distributions to charity from individual retirement plans (including IRAs) in 2012–2013, the Work Opportunity Tax Credit, the Section 179 deduction, tuition and fees expense deduction, and the exclusion of gain on the sale of small business stock, all of which are described in much greater detail below.

These tax changes are in addition to the new Medicare surtaxes. Beginning this year, the Patient Protection and Affordable Care Act imposes a 3.8% surtax on unearned income (e.g., passive income of individuals, trusts and estates) and a .9% tax on earned income (e.g., wages and self-employment income) in addition to current Social Security and Medicare taxes. The amount subject to the 3.8% tax is the lesser of net investment income or the excess of the taxpayers' modified adjusted gross income over $250,000 for taxpayers married filing jointly, $125,000 for married taxpayers filing separately and $200,000 for all other individual taxpayers.

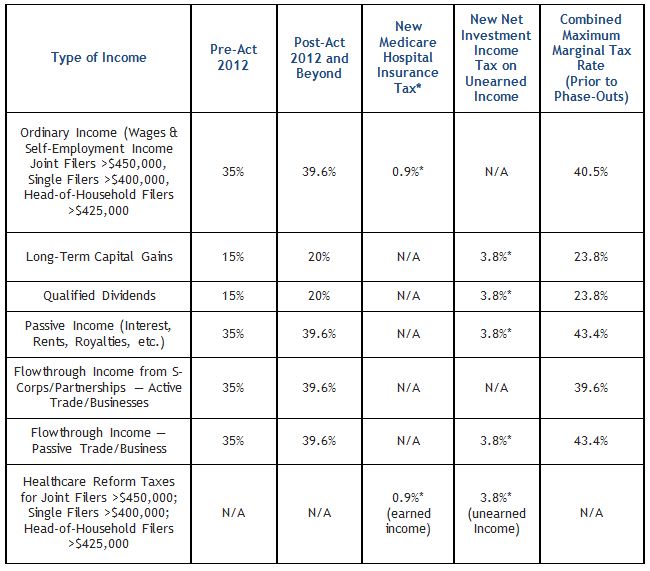

The following chart presents a quick summary of pre- and post-Act tax rates for "high income taxpayers" (generally defined as single taxpayers with income in excess of $400,000 and married taxpayers filing jointly with income in excess of $450,000 and head-of-household taxpayers with incomes in excess of $425,000).

*The New Medicare Hospital Insurance Tax and the New Net Investment Income Tax on Unearned Income applies to income in excess of $200,000 for single taxpayers and $250,000 for married taxpayers filing jointly. For taxpayers subject to the net investment income tax, the effective rate of tax will be 23.8%.

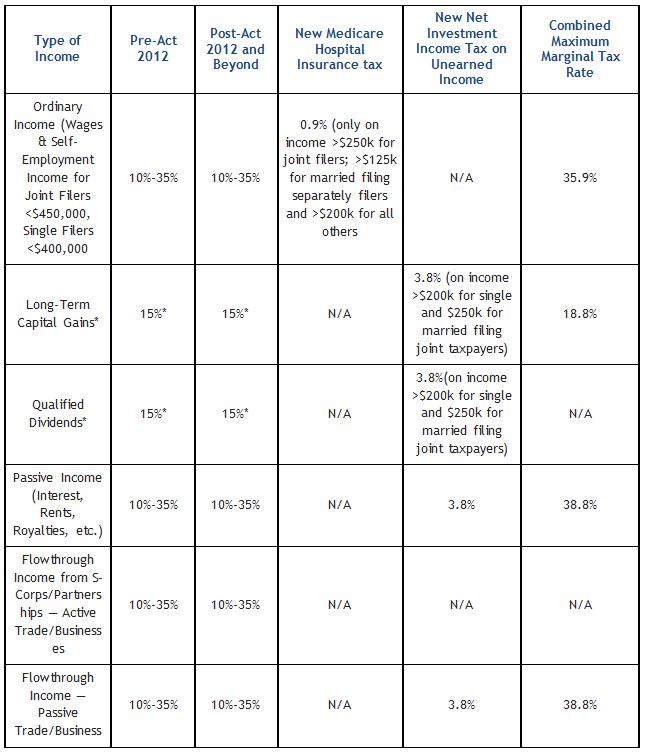

The following chart presents a quick summary of pre- and post-Act tax rates for individuals with incomes below the ranges indicated in the chart above, including retention of the favorable 15% tax rate for capital gains and qualified dividends for individuals earning less than $200,000 a year and households making less than $250,000.

* The zero tax rate on capital gains and dividend income is retained for taxpayers in the 10% and 15% tax brackets.

Notable Legislative Changes:

Individual Provisions Snapshot

- Individual Tax Rates

For single taxpayers with income above $400,000, ($450,000 for married taxpayers filing jointly, and $425,000 for heads of household) a 39.6% tax rate now applies. For taxpayers below these thresholds, the 10% through 35% rates remain the same.

- Capital Gains and Dividend Rates

For taxpayers exceeding the thresholds noted above, the maximum capital gain and dividend rate rises to 20%, from 15%. With the additional and new surtax on investment income, the combined marginal rate for individuals and couples with income above the $400,000/$450,000 thresholds is 23.8%. For taxpayers with incomes below these thresholds, the tax rate remains at 15%. The tax rate is zero for those taxpayers in the 10% and 15% tax brackets.

- The Personal Exemption Phase-out

For tax years beginning in 2013, the previously suspended PEP is reinstated with a starting adjusted gross income (AGI) threshold of $300,000, $275,000, $250,000 and $150,000 for joint filers and surviving spouses, heads-of-household, single filers and married taxpayers filing separately, respectively. Under the phase-out, the total amount of exemptions that can be claimed by a taxpayer subject to the limitation is reduced by 2% for each $2,500 (or portion thereof) by which the taxpayer's AGI exceeds the applicable threshold. These amounts are inflation-adjusted for tax years after 2013.

- Itemized Deduction Limitations

For tax years beginning in 2013, the previously suspended limitation on itemized deductions is reinstated with a starting threshold of $300,000 for joint filers and surviving spouses, $275,000 for heads of household, $250,000 for single filers and $150,000 for married taxpayers filing separately. For taxpayers subject to this limitation, the total amount of itemized deductions is reduced by 3% of the amount by which the taxpayer's AGI exceeds the threshold amount, with the reduction not to exceed 80% of the otherwise allowable itemized deductions. These dollar amounts are inflation-adjusted for tax years after 2013.

- The Alternative Minimum Tax (AMT)

Taxpayers have finally received permanent AMT relief. Prior to the Act, the individual AMT exemption amounts for 2012 were $33,750 for single taxpayers, $45,000 for joint filers and $22,500 for married persons filing separately. Retroactively effective for tax years beginning after 2011, the Act permanently increases these exemption amounts to $50,600 for single taxpayers, $78,750 for joint filers and $39,375 for married persons filing separately. In addition, for tax years beginning after 2012, it indexes these exemption amounts for inflation and permits certain non-refundable personal credits to offset the entire regular AND AMT tax liability.

Individual Extenders Snapshot

The Act extends for five years the following items that were originally enacted as part of the American Recovery and Investment Tax Act of 2009 (which we previously wrote about here) and that were slated to expire at the end of 2012:

- The American Opportunity tax credit, which permits eligible taxpayers to claim a credit equal to 100% of the first $2,000 of qualified tuition and related expenses, and 25% of the next $2,000 of qualified tuition and related expenses (for a maximum tax credit of $2,500 for the first four years of post-secondary education with phase-outs continuing for single taxpayers with AGI between $80,000 and $90,000 and joint taxpayers with AGI between $160,000 and $180,000).

- Eased rules for qualifying for the refundable child credit.

The Act also extends the following items through 2013:

- The deduction for certain expenses, up to $250, incurred by elementary and secondary school teachers;

- The exclusion from income of discharge of qualified principal residence indebtedness, up to $2 million ($1 million for married taxpayers filing separately), which applied for discharges before January 1, 2013;

- The treatment of mortgage insurance premiums as qualified residence interest, which expired at the end of 2011;

- The option to deduct state and local general sales taxes, which expired at the end of 2011;

- The above-the-line deduction for qualified tuition and related expenses, which expired at the end of 2011; and

- The exemption for 100% of the gain on sales of certain small business stock (generally, stock held for five years issued by a qualified small business, which is, in general, a business with assets of no more than $50 million). The exemption generally is for 50% of the gain. However, the exempt amount had been increased to 100% for stock acquired after September 27, 2010, and before January 1, 2012. The Act extends this 100% exclusion to stock acquired through the end of 2013.

Business Provisions Snapshot

The following select business tax breaks are also modified and extended:

- 15-year straight line cost recovery for qualified leasehold improvements, qualified restaurant buildings and improvements, and qualified retail improvements is extended through 2014;

- Increased expensing limitations to $500,000 (with a $2 million investment limit) and treatment of certain real property as Code Sec. 179 property;

- The Code Sec. 41 research credit is modified and retroactively extended for two years through 2013;

- Employer wage credits for employees who are active duty members of the uniformed services is retroactively extended for two years through 2013;

- The Code Sec. 51 work opportunity tax credit is retroactively extended for two years through 2013 with an available credit of 40% of first-year wages up to $6,000 for hiring select individuals within targeted groups;

- Exclusion from a tax-exempt organization's unrelated business taxable income (UBTI) of interest, rent, royalties and annuities paid to it from a controlled entity is extended through December 31, 2013;

- Treatment of certain dividends of regulated investment companies (RICs) as "interest-related dividends" is extended through December 31, 2013;

- Exclusion of 100% (from 50%) of gain on certain small business stock acquired before January 1, 2014;

- Basis adjustment to stock of S corporations making charitable contributions of property in tax years beginning before December 31, 2013;

- The reduction in S corporation recognition period for built-in gains tax is extended through 2013, with a 10-year period instead of a five-year period; and

- Various empowerment zone tax incentives, including the designation of an empowerment zone and of additional empowerment zones, are extended through December 31, 2013.

Energy Provisions Snapshot

- The nonbusiness energy property credit for energy-efficient existing homes is retroactively extended for two years through 2013. A taxpayer can claim a 10% credit on the cost of: (1) qualified energy-efficiency improvements and (2) residential energy property expenditures, with a lifetime credit limit of $500 ($200 for windows and skylights);

- The alternative fuel vehicle refueling property credit is retroactively extended for two years through 2013. Taxpayers can claim a 30% credit for qualified alternative fuel vehicle refueling property placed in service through December 31, 2013, subject to the $30,000 and $1,000 thresholds;

- The credit for two- or three-wheeled plug-in electric vehicles is modified and retroactively extended for two years through 2013;

- Credits with respect to facilities producing energy from certain renewable resources under Code Sec. 45 is modified and extended one year. A facility using wind to produce electricity will be a qualified facility if placed in service before 2014;

- The credit for energy-efficient new homes is retroactively extended for two years through 2013; and

- The credit for energy-efficient appliances is retroactively extended for two years through 2013.

Pension Provision Snapshot

- Roth conversions are expanded. Prior to the Act, distributions from such traditional retirement accounts as 401(k) plans, 403(b) plans or 457(b) plans could be contributed directly to an employer-offered Roth account only when the worker separated from service, reached age 59-1/2 died or became disabled. For transfers after December 31, 2012, 401(k) plans, 403(b) plans or 457(b) plans can have Roth accounts that allow participants to save on a Roth basis. That is, participants can make after-tax contributions to the plan and all the principal and earnings are tax-free when distributed. This provision allows any amount in a non-Roth account to be converted to a Roth account in the same plan, whether or not the worker separated from service, reached age 59-1/2, died or became disabled. The amount converted would be subject to regular income tax of course, but Roth account benefits have now expanded from IRAs to 401(k) and similar plans.

- Provision to allow tax-free IRA distributions up to $100,000 per year to charitable organizations by individuals age 70-1/2 or older has been extended through 2013, including special provisions allowing taxpayers to treat certain distributions or transfers in 2013 as if made in December 31, 2012.

Estate and Gift Tax Provisions Snapshot

- The top federal estate, gift and GST tax rate will increase from 35% to 40%.

- The federal estate tax exemption will remain at $5 million and will be indexed for inflation (approximately $5.25 million for 2013), and will apply for estate, gift and GST purposes.

- Surviving spouses will continue to have access to unused estate tax exemption amounts for estate and gift tax purposes (but not GST tax purposes).

New Taxes Snapshot

In addition to the various provisions noted above, some new taxes also took effect January 1 as a result of 2010's healthcare reform legislation as we reported here in our Health Care Reform Legislation Alert.

Medical Care Itemized Deduction Threshold

The threshold for the itemized deduction for unreimbursed medical expenses has increased from 7.5% of AGI to 10% of AGI for regular income tax purposes. This is effective for all individuals, except, in the years 2013?2016, if either the taxpayer or the taxpayer's spouse has turned 65 before the end of the tax year, the increased threshold does not apply and the threshold remains at 7.5% of AGI.

Health Flexible Spending Arrangement

Effective for cafeteria plan years beginning after December 31, 2012, the maximum amount of salary reduction contributions that an employee may elect to have made to a flexible spending arrangement for any plan year is $2,500.

Additional Legislation Likely

As we noted, while the Act addressed the tax side of the fiscal cliff, it did not address all of the "fiscal cliff" issues, most notably sequestration or the automatic spending cuts, which were a huge sticking point with Republican lawmakers. Additional legislation will be needed before March 1, 2013, to address the automatic military and domestic cuts as well as the debt limit.

For Further Information

This Alert is intended to provide a quick update on the latest action by Congress. We would be happy to discuss with you tax-planning implications in light of these changes.

As additional major legislative developments take place, we are available to discuss the impact of a new or pending tax law on your personal or business situation.

For other tax and related topics, please visit our publications page located here or contact any of the practitioners in the Tax Accounting Group.

As required by United States Treasury Regulations, you should be aware that this communication is not intended by the sender to be used, and it cannot be used, for the purpose of avoiding penalties under United States federal tax laws.

Disclaimer: This Alert has been prepared and published for informational purposes only and is not offered, nor should be construed, as legal advice. For more information, please see the firm's full disclaimer.