Though the end of the year is quickly approaching, there is still time to take advantage of some of the opportunities afforded under this landmark new tax law to reduce your 2025 tax liability.

![]()

Key Planning Tips and Tax Strategies in a New Tax Environment

This year has been very busy legislatively, with the passage of Public Law No: 119-21, also known as HR 1 as well as the “One Big Beautiful Bill Act,” (OBBBA) whether fondly or with irony, signed into law by President Donald Trump on July 4, 2025. This bill has reshaped tax compliance and planning and presents a range of new challenges and opportunities to consider for the balance of 2025, 2026 and beyond.

With its passage, Congress extended many of the provisions contained in the Tax Cuts and Jobs Act of 2017 (TCJA) that were set to expire at the end of 2025, in many instances with modifications, and touched nearly every aspect of the tax code with significant implications for individuals, businesses, investors and nonprofits. The OBBBA also introduced new deductions, along with phaseouts for higher-income taxpayers, including new deductions for workers and seniors, tax relief and enhanced credits for families, gain deferrals and exclusions for investors, immediate tax deductions for businesses, tax simplification measures for small businesses and permanent extension of the gift and estate tax exclusion.

Examples of a few key provisions of the new tax law, creating tax-planning opportunities for 2025, 2026 and beyond, include:

- Expansion of the state and local tax (SALT) deduction cap;

- New tip, overtime, car loan interest and senior deductions;

- New charitable and itemized deduction limitations set to hit in 2026;

- Permanent extension of 100 percent bonus depreciation for businesses;

- Significant revisions to the qualified opportunity zone program, including enhanced rural incentives;

- Expansion and modification of qualified small business stock gain exclusions; and

- Immediate expensing of domestic research and development expenditures.

These changes, and many more, can be found below in our overview of the OBBBA: Discover How the OBBBA Changes Your Tax Planning for 2025 and 2026. This section also includes a helpful table with a summary of the most impactful changes as a result of this legislation. As the tax changes are quite extensive, we hope you find this condensed summary useful.

Though the end of the year is quickly approaching, there is still time to take advantage of some of the opportunities afforded under this landmark new tax law to reduce your 2025 tax liability. Our 2025 Year-End Tax Planning Guide highlights select and noteworthy tax strategies and potential planning opportunities to consider for this year and, in many cases, 2026. We also highlight hidden pitfalls.

While we do not expect major new tax legislation in 2026, with tax legislation, nothing is certain of course. There may be attempts to expand the SALT deduction and there certainly will be the correction of technical deficiencies and unintended consequences of the OBBBA. We continue to carefully monitor and study changing tax legislation and IRS guidance on enacted legislation. As major tax developments and opportunities emerge, we are always available to discuss the impact on your personal or business situation. Please keep a watchful eye on our Alerts published throughout the year, which contain information on tax developments and are designed to keep you informed while offering practical insights and tax-saving opportunities.

In this 2025 Year-End Tax Planning Guide prepared by the CPAs, attorneys and IRS-enrolled agents of the Tax Accounting Group of Duane Morris LLP, along with contributions from the trust and estate attorneys of our firm’s Private Client Services Practice Group, we walk you through the steps needed to assess your personal and business tax situation in light of both existing law and potential law changes and identify actions needed before year-end and beyond to reduce your 2025, 2026 and future tax liabilities.

We hope you find this complimentary guide valuable and invite you to consult with us regarding any of the topics covered or your own unique situation. For additional information, please contact me, Michael A. Gillen, at 215.979.1635 or magillen@duanemorris.com, John I. Frederick or the practitioner with whom you are regularly in contact.

Wishing you and your loved ones a joyful holiday season and a healthy, peaceful and successful New Year.

Michael A. Gillen

Tax Accounting Group

About Duane Morris LLP

Duane Morris LLP, a law firm with more than 900 attorneys in offices across the United States and internationally, is asked by a broad array of clients to provide innovative solutions to today’s legal and business challenges. Evolving from a partnership of prominent lawyers in Philadelphia over a century ago, Duane Morris’ modern organization stretches from the U.S. to the U.K. and across Asia. Throughout this global expansion, Duane Morris has remained committed to preserving its collegial, collaborative culture that has attracted many talented attorneys. The firm’s leadership, and outside observers like the Harvard Business School, believe this culture is truly unique among large law firms and helps account for the firm continuing to prosper throughout changing economic and industry conditions. Most recently, Duane Morris has been recognized by BTI Consulting as both a client service leader and a highly recommended law firm. Additionally, multiple Duane Morris offices have received recognition as top workplaces for consecutive years.

At a Glance

- Offices in 22 U.S. cities in 12 states and the District of Columbia

- Offices in Asia and the United Kingdom and liaisons in Latin America

- More than 1,600 people

- More than 900 lawyers

- AM Law 100 since 2001

In addition to legal services, Duane Morris is a pioneer in establishing independent affiliates providing nonlegal services to complement and enhance the representation of our clients. The firm has independent affiliates employing more than 100 professionals engaged in other disciplines, such as the tax, accounting and litigation consulting services offered by the Tax Accounting Group.

About the Tax Accounting Group

The Tax Accounting Group (TAG) was the first ancillary practice of Duane Morris LLP and is one of the largest tax, accounting and litigation consulting groups affiliated with any law firm in the United States. Approaching our 45th anniversary in 2026, TAG has an active and diverse practice with over 60 service lines in more than 45 industries, serving as the entrusted advisor to clients in every U.S. state and 25 countries through our regional access, national presence and global reach. In addition, TAG continues to enjoy impressive growth year over year, in large part because of our clients’ continued expression of confidence and referrals. To learn more about our service lines and industries served, please refer to our Quick Reference Service Guide.

TAG’s certified public accountants, certified fraud examiners, attorneys, financial consultants and advisors provide a broad range of cost-effective tax compliance, planning and consulting services as well as accounting, financial and management advisory services to individuals, businesses, estates, trusts and nonprofit organizations. TAG also provides an array of litigation consulting services to lawyers and law firms representing clients in regulatory and transactional matters and throughout various stages of litigation. Our one-of-a-kind CPA and lawyer platform allows us to efficiently deliver one-stop flexibility, customization and specialization to meet each of the traditional, advanced and unique needs of our clients, all with the convenience of a single-source provider.

We serve clients of all types and sizes, from high-net-worth individuals to young and emerging professionals, corporate executives to entrepreneurs, multigenerational families to single and multifamily offices, mature businesses to startups, global professional service firms to local companies, and foundations and nonprofits to governmental entities. We assist clients with a wide range of services, from traditional tax compliance to those with complex and unique needs, conventional tax planning to advanced strategies, domestic to international tax matters for clients working abroad as well as foreign businesses and individuals working in the United States, traditional civil tax representation to those criminally charged, those in need of customary accounting, financial and management advisory services, to those requiring innovative consulting solutions and those in need of sophisticated assistance in regulatory and transactional matters and throughout various stages of litigation.

With our service mission to enthusiastically provide effective solutions that exceed client expectations, and the passion, objectivity and deep experience of our talented professionals, including our dedicated senior staff with an average of over 25 years working together as a team at TAG (with a few having more than 35 years on our platform), TAG is truly distinctive. Being “truly distinctive and positively effective” is not just our TAGline, it is our passion.

Whether you are a client new to TAG or are among the many who have been with us for nearly 45 years, it is our honor and privilege to serve you.

For the first time in nearly a decade, a significant portion of the tax code is not facing imminent sunset or expiration. We have greater tax certainty in the near term than we have enjoyed in years. However, this year, with Congress setting the precedent of scoring costs based on a current policy baseline as opposed to a current law baseline, the long-term future of tax law has never been more uncertain. Future congresses will be able to change tax law much more easily—and on a permanent basis.

For the past several years, Congress has needed continuing resolutions to pass budgets, and we have recently endured the longest government shutdown in history. As a result, we expect very little bipartisan cooperation moving forward, with few tax bills introduced or progressing, other than potential adjustments to the SALT limitation or technical corrections of the OBBBA. Overall, we do not anticipate the introduction of new major tax legislation pertaining to 2026.

Accordingly, there has never been a better time to plan. As we approach year-end, we are again fielding calls, outreaches and multiyear tax modeling requests from existing and new clients regarding year-end as well as multiyear tax planning strategies available to individuals, businesses, estates, trusts and nonprofits.

These discussions have centered around the new tax law and how it impacts each client’s individual scenario. As enacted, the OBBBA accomplished six main objectives:

- Permanently (for now) extending the key tax breaks under the TCJA set to expire at the end of 2025;

- Permanently (for now) eliminating and reducing certain deductions suspended or reduced under the TCJA;

- Introducing new tax provisions and deductions of its own, primarily to support working Americans;

- Introducing new limitations on existing deductions to pay for tax cuts;

- Enhancing existing deductions and credits; and

- Eliminating Biden-era energy credits.

In summary, the OBBBA:

- Extended TCJA tax benefits such as lowered individual tax rates;

- Increased standard deductions;

- Added larger alternative minimum tax exemptions;

- Solidified the qualified business income deduction for pass-through entities;

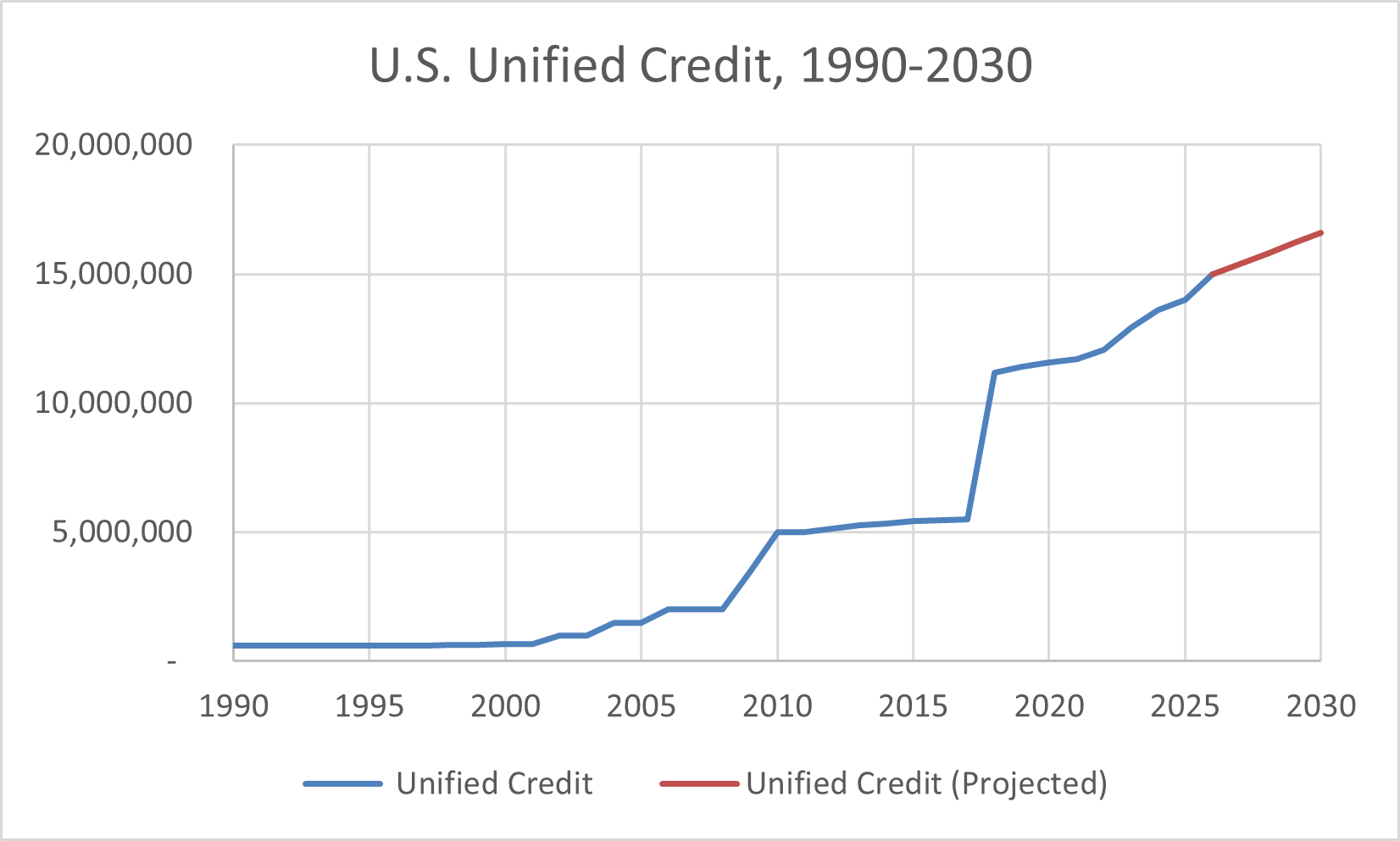

- Doubled the estate, gift and generation-skipping transfer tax exemption to $15 million for 2026;

- Eliminated deductions that were initially suspended by the TCJA, including the Pease limitation on itemized deductions, miscellaneous itemized deductions subject to the 2 percent floor, and personal exemptions (though the Pease limitation was replaced with a new 2/37ths limitation, see strategy 2);

- Modified several itemized deductions such as the SALT deduction limitation and the mortgage interest deduction limitation, however, with both having taxpayer-friendly enhancements;

- Introduced new deductions including “no tax on tips,” “no tax on overtime,” the senior deduction and the car loan interest deduction, all subject to limitations and phaseouts based on income;

- Added additional limitations for both the individual and corporate charitable contribution deductions (0.5 percent and 1 percent floors for each, respectively), gambling losses (only allowed to deduct 90 percent of losses), and itemized deductions generally (2/37ths limitation);

- Enhanced existing credits, such as raising the child tax credit to $2,200 and increasing the credit percentage and income phaseout ranges for the child and dependent care credit; and

- Effectuated the early termination of a number of energy credits for individuals and businesses, including residential energy credits, vehicle credits, and solar and wind credits.

These robust changes to the tax code offer a litany of opportunities to plan for tax savings, while also creating new pitfalls. While you can depend on TAG for cost-effective tax compliance, planning and consulting services—as well as critical advocacy and prompt action in connection with your long-term personal and business objectives—we are also available for any immediate or last-minute needs you may have or those that Congress may legislate that impact your personal or business tax situation.

With the same tax rates expected for 2026, the tried-and-true strategy of deferring income and accelerating deductions may be beneficial in reducing tax obligations for most taxpayers in 2025. With minor exceptions, December 31 is the last chance to develop and implement your tax plan for 2025, but it is certainly not the last opportunity.

For example, if you expect to be in the same tax bracket in 2026 as 2025, deferring taxable income and accelerating deductible expenses can possibly achieve overall tax savings for both 2025 and 2026. However, by reversing this technique and accelerating 2025 taxable income and/or deferring deductions to plan for a possible higher 2026 tax rate, your two-year tax savings may be higher. This may be an effective strategy for you if, for example, you have charitable contribution carryovers to absorb, your marital status will change next year or your head of household or surviving spouse filing status ends this year. This analysis can be complex, and you should seek professional guidance before implementation. Examine our “Words of Caution” section below for additional thoughts in this regard.

This guide provides practical insights and tax planning strategies for corporate executives, businesses, individuals―including high-income and high-wealth families―nonprofit entities and estates and trusts. We hope that this guide will help you leverage the tax benefits available to you presently, reinforce the tax savings strategies you may already have in place, or develop a tax-efficient plan for 2025 and 2026.

To help you prepare for year-end, below is a reference table of key OBBBA changes with a reference to our corresponding planning strategy number, organized by several common individual scenarios, which can help you reach your tax-minimization goals—as long as you act before the clock strikes midnight on New Year’s Eve. Not all of the action steps will apply in your particular situation, but you could likely benefit from many of them. You may want to consult with us to develop and tailor a customized plan with defined multiyear tax modeling to focus on the specific actions that you are considering. We will be pleased to help you analyze the options, avoid pitfalls and decide on the strategies that are most effective for you, your family and your business.

As we predicted last year, 2025 was a watershed year for tax policy in the United States. The OBBBA is one of the biggest tax overhauls in years and touches almost every part of the tax system—individuals, families, small businesses and even multinational companies. At its core, the legislation attempts to keep in place many of the tax cuts Americans have used since 2017, while also expanding certain benefits and tightening others. Over the past year, everyone else (not only tax practitioners) has learned what the term “SALT” meant—as the state and local tax deduction limitation got a much-needed increase for some from $10,000 to $40,000. Beginning in 2026, tax brackets will stay lower than they were scheduled to be, major family credits get a boost and several long-awaited changes, like broader 529 benefits and Form 1099 threshold increases, finally arrive.

For families, the bill increases the child tax credit, expands the child and dependent care credit, and makes it easier to save for education or pay for student loans using employer benefits. It also creates taxpayer-friendly provisions like no tax on tips or overtime pay, larger standard deductions and new “Trump accounts” for family savings. At the same time, some longstanding deductions, including unreimbursed employee expenses and certain casualty losses, are permanently (for now) eliminated for most taxpayers, unless very specific conditions are met.

For business owners, OBBBA extends the 20 percent qualified business income deduction, restores full expensing for domestic R&D, provides more favorable rules for depreciation and investment, and adjusts the interest-deduction limits in a way that will matter for highly leveraged operations. There are also changes to fringe benefits: some become more generous (i.e., employer-provided child care), while others (i.e., employer-provided meals) become more limited or nondeductible.

In short, the OBBBA impacted a broad swathe of the tax code, and the table below summarizes its most important impacts, with a reference to a deeper discussion on those topics later in this guide.

Quick-Look Reference Table of Key OBBBA Changes

|

OBBBA Change |

Impact |

When |

Strategy |

|

0.5% floor for charitable deductions |

A portion of charitable gifts are no longer deductible for itemizers. |

2026 |

1 |

|

2/37ths itemized deductions limitation |

Itemized deductions are less valuable for taxpayers in the highest bracket. |

2026 |

2 |

|

$40,000 SALT cap |

The SALT deduction cap is temporarily increased and is reduced to $10,000 at higher incomes. |

2025 |

4 |

|

$6,000 senior deduction |

Additional deduction is available to seniors, subject to phaseout. |

2025 |

5 |

|

No tax on tips |

Tipped workers can deduct up to $25,000 of eligible tips, subject to phaseout. |

2025 |

6 |

|

No tax on overtime |

Workers can deduct up to $12,500 of eligible overtime, subject to phaseout. |

2025 |

7 |

|

$10,000 car loan interest deduction |

Personal new car loan interest is now deductible, for purchases of new domestic cars. |

2025 |

8 |

|

Charitable deduction for nonitemizers |

Nonitemizers can deduct up to $1,000 (single)/$2,000 (married) of cash donations in a calendar year. |

2026 |

9 |

|

90% gambling loss limitation |

Gambling losses are now limited to 90% of losses, or 100% of winnings, whichever is less. |

2026 |

10 |

|

Opportunity zone gain deferral |

The opportunity zone program is made permanent with eligible investments taking place on a rolling 10-year basis. |

2027 |

11 |

|

Trump accounts |

New tax-advantaged custodial accounts for children. |

2026 |

12 |

|

Energy credits |

Most home, vehicle and clean-energy credits will sunset in/after 2025. |

2025 - 2027 |

13 |

|

Qualified production property |

New domestic real property generally used in agriculture or manufacturing qualifies for 100% bonus depreciation. |

2025 |

14 |

|

100% bonus depreciation |

100% bonus depreciation is made permanent, allowing the write-off of qualifying assets. |

2025 |

15 |

|

1% floor for corporate charitable giving |

Charitable deductions by corporations are only allowed for the amounts above 1% of income. |

2026 |

16 |

|

1099-MISC/NEC thresholds |

1099-MISC and 1099-NEC threshold will be raised from $600 to $2,000 in 2026; fewer small businesses will have to prepare 1099s. |

2026 |

17 |

|

1099-K threshold |

1099-K threshold is raised to $20,000 or 200 transactions per year; fewer 1099-Ks issued to small businesses. |

2025 |

18 |

|

Disaster-loss deduction |

Above-the-line disaster-loss deduction is made permanent and will now include state-declared disasters. |

2026 |

19 |

|

New student-loan repayment programs |

New 2026 repayment plan replaces old IDR repayment system and tries to better tie payments to income. |

2026 |

21 |

|

Employee retention credit |

IRS now has six years to audit ERC claims and can assess additional penalties on ERC promoters. |

2025 |

22 |

|

Standard deduction |

The larger standard deduction has been permanently extended and indexed for inflation. |

2025 |

24 |

|

Child and dependent care credit |

Dependent care credit expanded with enhanced benefits for low- and middle-income taxpayers in 2026. |

2026 |

27 |

|

Child tax credit |

The credit has been increased to $2,200 per qualifying child and indexed for inflation. |

2025 |

28 |

|

Adoption credit |

The adoption credit increased, with partial refundability added to the credit. |

2025 |

29 |

|

Mortgage-insurance premiums deduction |

PMI premiums are permanently deductible again beginning in 2026. |

2026 |

32 |

|

Qualified small business stock |

The gain exclusion has been increased, as has the asset maximum of the corporation, and holding periods of less than five years offer greater benefit. |

2025 |

41 |

|

529 plans |

Qualified expenses now include more types of expenses, vocational expenses and $20,000 of K-12 expenses per year (up from $10,000). |

2026 |

60 |

|

Alternative minimum tax (AMT) |

Permanent AMT relief, but a quicker phase-out means that AMT will capture more higher-income taxpayers. |

2026 |

72 |

|

Qualified business income (QBI) deduction |

The QBI deduction was extended permanently, and more income allowed before phaseout of the deduction. |

2026 |

83 |

|

Excess business losses |

The limitation on business loss deductions was permanently extended. |

2025 |

87 |

|

Business interest deductions |

Several changes to calculation of the deduction, but most importantly, depreciation and amortization are now added back to taxable income, resulting in larger deductions for many. |

2026 |

88 |

|

Employer provided meals |

Employer-provided meals for the convenience of the employer and snacks become nondeductible. |

2026 |

94 |

|

R&D expenses |

Domestic R&D can now be immediately deducted rather than amortized over 15 years. |

2025 |

97 |

|

Home office deduction |

Employees can no longer deduct employee expenses, including home office. |

2025 |

104 |

|

Employer child care credit |

Credit for employers increased from $150,0000 to $500,0000, among other broadening measures. |

2026 |

108 |

|

Hobby expenses |

Hobby expenses are now nondeductible permanently. |

2025 |

115 |

|

Employer student-loan repayment |

Employer student-loan assistance exclusion from gross income was permanently extended and indexed for inflation. |

2025 |

123 |

|

Estate and gift tax |

Estate and gift tax exemption permanently raised to an inflation indexed $15 million per individual. |

2026 |

130 |

|

Foreign tax credit |

Revised sourcing rules may reduce credit for certain foreign taxes. |

2025 |

148 |

Garnering many of the headlines during election season and as the bill made its way through Congress were the new tax deductions based on President Trump’s campaign promises to exempt certain categories of income. While exemptions were ultimately not in the cards, the final version of the OBBBA contained four new deductions that addressed the themes discussed during the election that shared many similarities. Though each will be discussed in greater depth at strategies 5-8 herein, see this side-by-side comparison of the four new provisions and who they potentially benefit, including modified adjusted gross income (MAGI) phaseouts.

New Individual Deductions Under the OBBBA

|

New Deduction |

Maximum Annual Deduction |

MAGI Phaseout Range (Single) |

MAGI Phaseout Range (MFJ) |

|

Senior (65+) |

$6,000 per eligible individual |

$75,000 - $175,000 |

$150,000 - $250,000 |

|

Tips |

$25,000 |

$150,000 - $400,000 |

$300,000 - $550,000 |

|

Overtime |

$12,500 if single; $25,000 if filing jointly |

$150,000 - $275,000 |

$300,000 - $550,000 |

|

Car-loan interest |

$10,000 |

$100,000 - $150,000 |

$200,000 - $250,000 |

The remaining days of 2025 (as well as the first four and a half months of 2026 in some circumstances) offer a great opportunity for you to review these OBBBA changes with your tax advisor and determine which strategies may apply. Of course, many of the same perennial planning strategies remain available as well. However, your changing circumstances may warrant a new look at some tried and true strategies that may not have been applicable in the past.

Whether you should accelerate taxable income or defer tax deductions between 2025 and 2026 largely depends on your projected highest (aka marginal) tax rate for each year. While the highest official marginal tax rate for 2025 is currently 37 percent, you might pay more tax than in 2024 even if you were in a higher tax bracket due to credit fluctuations, compositions of capital gains and dividends, and a myriad of other reasons.

The chart below summarizes the most common 2025 tax rates together with the corresponding taxable income levels presently in place. Effective management of your tax bracket can provide meaningful tax savings, as a change of just $1 in taxable income can shift you into the next higher or lower bracket. These differences can be further exacerbated by other income thresholds throughout the Internal Revenue Code, discussed later in this guide, such as those for determining eligibility for the child tax credit and qualified business income deductions, among others. Income deferral and acceleration, while being mindful of bracket thresholds, can be accomplished through numerous income strategies discussed in this guide, such as retirement distribution planning, bonus acceleration or deferral, and harvesting of capital gains and losses.

2025 Federal Ordinary Income Tax Rate Schedule

|

Tax Rate |

Single |

Head of Household |

Married Couple |

|

10% |

$0 – $11,925 |

$0 – $17,000 |

$0 – $23,850 |

|

12% |

$11,926 – $48,475 |

$17,001 – $64,850 |

$23,851 – $96,950 |

|

22% |

$48,476 – $103,350 |

$64,851 – $103,350 |

$96,951 – $206,700 |

|

24% |

$103,351 – $197,300 |

$103,351 – $197,300 |

$206,701 – $394,600 |

|

32% |

$197,301 – $250,525 |

$197,301 – $250,500 |

$394,601 – $501,050 |

|

35% |

$250,525 – $626,350 |

$250,500 – $626,350 |

$501,051 – $751,600 |

|

37% |

Over $626,350 |

Over $626,350 |

Over $751,600 |

While reviewing this guide, please keep the following in mind:

- Never let the tax tail wag the financial dog, as we often preach. Always assess economic viability. This guide is intended to help you achieve your personal and business financial objectives in a “tax efficient” manner. It is important to note that proposed transactions should make economic sense in addition to generating tax savings. Therefore, you should review your entire financial position prior to implementing changes. Various nontax factors can influence your year‑end planning, including a change in employment, your spouse reentering or exiting the work force, the adoption or birth of a child, a death in the family or a change in your marital status. It is best to look at your tax situation for at least two years at a time with the objective of reducing your tax liability for both years combined, not just for 2025. In particular, multiple years should be considered when implementing “bunching” or “timing” strategies, as discussed throughout this guide.

- Be very cautious about accelerated timing causing you to lose too much value, including the time value of money. That is, any decision to save taxes by accelerating income must consider the possibility that this means paying taxes on the accelerated income earlier, which would require you to forego the use of money used to satisfy tax liabilities that could have been otherwise invested. Accordingly, the time value of money can make a bad decision worse or, hopefully, a good decision better―a delicate balance, indeed.

- While the traditional strategies of deferring taxable income and accelerating deductible expenses will be beneficial for many taxpayers, you can often achieve overall tax efficiency by reversing this technique. For example, waiting to pay deductible expenses such as mortgage interest until 2026 would defer the tax deduction to 2026. Or, waiting to pay SALT until 2026 if you have already exceeded your SALT deduction cap in 2025 could also be worthwhile. You should consider deferring deductions and accelerating income if you expect to be in a higher tax bracket next year, you have charitable contribution carryovers to absorb, your marital status will change next year or your head of household or surviving spouse filing status ends this year. This analysis can be complex, and you should seek professional guidance before implementation.

- Both individuals and businesses have many ways to “time” income and deductions, whether by acceleration or deferral. Businesses, for example, can make different types of elections that affect the timing of significant deductions. Faster or slower depreciation, including electing in or out of bonus depreciation, is one of the most significant. This type of strategy should be considered carefully as it will not simply defer a deduction into the following year but can push the deduction out much further or spread it over a number of years.

- For quite some time, the alternative minimum tax (AMT) was unimportant for many taxpayers. OBBBA may have changed that starting in 2026. The AMT is a separate, yet parallel, federal income tax calculation designed to ensure that certain high-income individuals and corporations pay at least a minimum amount of tax, even if they have many deductions or credits that would otherwise significantly lower their regular income tax. If the AMT exceeds your regular tax, you owe the larger AMT amount. For 2026 and beyond, AMT exemptions for higher-income taxpayers may be phased out faster resulting in more taxpayers owing the AMT for 2026 and beyond. See strategy 72.

With these words of caution in mind, the following are observations and specific strategies that can be employed in the waning days of 2025 regarding income and deductions for the year, where the tried-and-true strategies of deferring taxable income and accelerating deductible expenses will result in maximum tax savings.

Below is a quick and easy reference guide outlining practical action steps that can help you reach your tax-minimization goals, as long as you act before year-end. In this guide, we have identified the best possible action items for you to consider, depending on how your income shapes up as the year draws to a close.

Not all of the action steps will apply in your particular situation, and some may be better for you than others. In addition, several steps can be taken before year-end that are not necessarily “quick and easy” but could yield even greater benefits. For example, perhaps this is the year that you finally set up your private foundation or a donor-advised fund to achieve your charitable goals (see strategies 126 and 35, respectively) or maybe you decide it is time to review your estate plan in order to utilize the current lifetime gift and estate tax exemption (see strategies 130-145). Consultation to develop and tailor a customized plan focused on the specific actions that should be taken is paramount.

To help guide your thinking and planning in light of the multiple situations in which you may find yourself at year-end, we have compiled the below quick-strike action steps that follow different themes depending on several common situations. You may wish to consider several potential actions and identify the most relevant and significant steps for your particular situation.

Quick-Strike Action Step Themes

|

Situation |

Reason |

Theme |

Potential Action |

|

You expect to pay higher ordinary income tax rates in 2026 |

Increased income—either from a liquidation event, entering the workforce, or a large bonus in 1Q26 Getting married, subject to marriage penalty Head of household or surviving spouse filing status ends after 2025 |

Accelerate income into 2025 Defer deductions until 2026 |

Accelerate installment sale gain into 2025 (strategy 117) Defer SALT payments to 2026 (strategy 31) Bunch itemized deductions in 2026 (strategy 33) Recognize bond interest (strategy 42) Reduce or delay pre-tax retirement contributions (strategy 53) |

|

You expect to pay lower ordinary income tax rates in 2026 |

Retirement Decreased income Head of household status eligibility in 2026 A child escaping the “kiddie tax” regime in 2026

|

Accelerate deductions into 2025 Defer income until 2026 |

Defer income until 2026 (strategy 23) Maximize medical deductions in 2025 (strategy 30) Prepay January mortgage (strategy 32) Consider deduction limits for charitable contributions (strategies 34 and 35) Bunch itemized deductions in 2025 (strategy 33) Sell passive activities (strategy 51) Increase basis in partnership and S corporation to maximize losses (strategy 52) Maximize pre-tax retirement contributions (strategy 53) Maximize contributions to FSAs and HSAs (strategies 66 and 67) Defer debt cancellation events (strategy 71) Delay retirement plan distributions or contribute retirement distributions to charity (strategy 58) |

|

You have high capital gains in 2025 |

Business or property sold An investment ends Employee stock is sold |

Reduce or defer gains |

Invest in qualified opportunity zones (strategies 11 and 20) Invest in Section 1202 small business stock (strategy 41) Perform a like-kind exchange (strategy 48) Harvest losses (strategy 40) |

|

You have low capital gains in 2025 |

Carry forward losses Large current year loss |

Increase capital gains |

Maximize preferential gains rates (strategy 37) Sell principal residence (strategy 47) Harvest gains without regard to wash sale rules (strategy 39) |

1. Accelerate charitable contributions into 2025 to avoid the new charitable floor in 2026. As a result of the OBBBA, beginning in tax year 2026, charitable contributions deducted as an itemized deduction will be subject to a “floor” of 0.5 percent of a taxpayer’s adjusted gross income (AGI). This means that taxpayers can only deduct the portion of their total charitable contributions that exceed this floor. For example, if a taxpayer’s AGI is $500,000 and the total cash contributions made for the year was $30,000, they would only be able to deduct $27,500 for the year ($500,000 x 0.5 percent = $2,500; $30,000 - $2,500 = $27,500).

This limitation also operates in conjunction with the charitable contribution “ceiling” already in place. For most charitable contributions made in the form of cash, other than to a private foundation, the limitation on the deduction is 60 percent of the taxpayer’s AGI. If total charitable contributions exceed the 60 percent ceiling, the excess is disallowed as a deduction for the current year and is carried forward to the following year.

Under OBBBA, the portion of the charitable contributions disallowed by the 0.5 percent floor is also carried forward if total contributions exceed the 60 percent ceiling. In the first example, the $2,500 that is disallowed is permanently lost, since total charitable contributions do not exceed the ceiling. For a taxpayer with AGI of $500,000 and total cash contributions of $315,000 for the year (assuming all are subject to the 60 percent ceiling), the total deduction for the year is $297,500, with $17,500 carried forward to the following year, as demonstrated below:

- 60 percent of AGI limitation (ceiling) → $500,000 (AGI) x 60 percent = $300,000

- Deductible amount → $300,000 (ceiling) - $2,500 (floor) = $297,500

- Carryforward amount → $315,000 (total cash contributions) - $297,500 (current year deduction) = $17,500

Overview of New Rules for Charitable Giving for Individual Taxpayers Starting in 2026

|

Total Charitable Contributions |

Current Year Deduction

|

Carryforward to the Following Year |

|

Contributions < 0.5% of AGI |

None |

None |

|

0.5% of AGI < Contributions < 60% of AGI |

Current year contributions less 0.5% of AGI |

None |

|

Contributions > 60% of AGI |

60% of AGI (ceiling) less 0.5% of AGI (floor) = 59.5% of AGI |

Current year contributions not deducted in the current year (total contributions less 59.5% of AGI) |

2. Shift itemized deductions into 2025 to avoid the 2/37ths reduction in 2026. The OBBBA ended the suspended “Pease limitation” (named after the late Congressman Donald Pease, which was an overall limitation on the amount of itemized deductions that high-income taxpayers can claim on their federal income taxes) that was in effect prior to tax year 2018 and replaced it with a new provision that limits the tax benefit of itemized deductions beginning in 2026, and is informally being referred to as the “2/37ths limitation.” With this new limitation for high-income taxpayers, itemized deductions are reduced by 2/37ths of the total amount of itemized deductions or the amount of the taxable income before itemized deductions exceeding the 37 percent bracket threshold, whichever is less. Basically, this limitation limits the benefit itemized deductions provide to taxpayers in the highest income tax bracket. For taxpayers in the highest (37 percent) bracket, itemized deductions will only have a tax benefit of 35 percent.

In 2025, if a taxpayer has taxable income before itemized deductions of $1.5 million, and total itemized deductions of $100,000, the actual tax saved is 37 percent of the itemized deductions—in this case $37,000. However, in 2026, after applying this new limitation, the tax benefit is only $35,000, as follows: $100,000 x 2/37 = $5,405 → $100,000 - $5,405 = $94,595 → $94,595 x 0.37 (37 percent) = $35,000. Total itemized deductions are reduced to $94,595, and in turn, this limitation results in the same tax savings to the taxpayer in the higher bracket as to the taxpayer in the second highest bracket. See the chart below to determine what amount is subject to this limitation:

Calculation of 2/37ths Limitation Based on Amount of Taxable Income

|

Taxable Income Before Itemized Deductions |

Total Itemized Deductions Before Limitation |

Amount Subject to 2/37ths Limitation |

|

Taxable income < highest bracket threshold |

N/A

|

N/A

|

|

Taxable income > highest bracket threshold |

Itemized deductions < taxable income less highest bracket threshold |

Total itemized deductions

|

|

Taxable income > highest bracket threshold |

Itemized deductions > taxable income less highest bracket threshold |

Taxable income less highest bracket threshold |

It is important to note that this provision does not carve out any exceptions for income taxed at preferential rates. If income taxed at ordinary rates is below the highest bracket threshold, but income taxed at preferential rates brings total taxable income into the highest bracket, this limitation will still apply even though the tax savings is less than 37 percent. In such situations, the limitation will result in itemized deductions having a tax savings of even less than 35 percent of the total.

3. Brace for a potential hit to your take-home pay if you are 50 or older (though it could be a good thing in the long run). Beginning in 2026, retirement plan catch-up contributions must be made on an after-tax (Roth) basis if the taxpayer’s wages exceeded $145,000 in the prior year (indexed for inflation).

This after-tax requirement only affects participants of employer-sponsored 401(k) plans age 50 and over by the end of the tax year who contribute what are known as “catch-up contributions” to their 401(k)-plan account. Catch-up contributions are contributions in addition to the standard statutory contribution limit for the year. The regular 401(k) contribution limit for 2025 is $23,500 and the catch-up contribution limit is $7,500. This means that an individual participant who turns 50 in 2025 can contribute a total of $31,000 in 2025.

Starting in the year 2025, participants aged 60-63 are eligible to make a higher catch-up contribution of $11,250. This means that an individual who is between 60 and 63 at the end of 2025 is able to contribute a total of $34,750 during the year, rather than $31,000.

Beginning in 2026, both the standard catch-up and the higher catch-up are subject to this new after-tax rule. Since it is entirely optional for a plan to offer participants the ability to make catch-up contributions, some employers have already amended their plan documents to no longer permit participants from making catch-up contributions to avoid compliance with the new rule.

However, it is important to understand that the after-tax rule is based only on the participant’s prior year Federal Insurance Contributions Act (FICA) wages from the plan sponsor (the employer which the 401(k) plan is through). This means that if their FICA wages from the plan sponsor were equal to or less than $145,000 in 2025, but they had FICA wages from another employer resulting in total FICA wages over $145,000, the employee would not be subject to this rule and would still be able to make before-tax catch-up contributions in 2026. There are limited exceptions and somewhat nuanced rules for multiple employers of a controlled group, but generally the employer is not responsible for collecting other types of data from their employees to comply with this new rule.

For any W-2 employee that this affects, you may want to consult with your employer to determine what you will need to do to (if anything) to change your contribution allocations. The employer may automatically designate applicable catch-up contributions as Roth, or you may no longer have the ability to make catch-up contributions entirely.

4. Unlock a larger SALT deduction for 2025. The SALT deduction limit has been a hot topic for a number of years since it originated in the 2017 TCJA. Prior to the TCJA, no such limit existed and taxpayers could deduct the full amount of SALT paid during the year. However, the TCJA limited the amount of SALT claimed as an itemized deduction to $10,000 (or $5,000 in the case of taxpayers married filing separately). This provision went into effect beginning for tax year 2018 and was originally scheduled to sunset after 2025.

During the 2024 campaign, President Trump indicated that he was in favor of eliminating this provision entirely, while other politicians believed it was necessary to leave the limitation in place in order to offset other tax cuts. The SALT provision that made it into the final version of the OBBBA is a bit of a compromise between the two.

The OBBBA did not eliminate the SALT limit but did temporarily modify it. Beginning for tax year 2025, the limit increases to $40,000 (or $20,000 in the case of taxpayers married filing separately) and is indexed to increase by 1 percent every year until 2030, when it is set to revert back to $10,000. This limit phases down by 30 percent of a taxpayer’s MAGI over $500,000 (or $250,000 in the case of taxpayers married filing separately), but never below the original $10,000 limit. So, essentially there is a modified MAGI phaseout range, which for taxpayers other than those who are married filing separately, is $500,000 - $600,000, as illustrated below.

SALT Deduction Cap Phaseout by MAGI

|

Tax Year |

SALT Deduction Cap |

Phaseout Range Begins at |

Phaseout Range Ends at |

|

2025 |

$40,000 |

$500,000 |

$600,000 |

|

2026 |

$40,400 |

$505,000 |

$606,333 |

|

2027 |

$40,804 |

$510,050 |

$612,730 |

|

2028 |

$41,212 |

$515,151 |

$619,191 |

|

2029 |

$41,624 |

$520,302 |

$625,716 |

|

2030 |

$10,000 |

N/A |

N/A |

If your income fluctuates around the phaseout range, to the extent possible, you should time your tax payments so that you pay more SALT in a year when your income is lower and you are subject to a higher limitation.

5. Leverage the new senior deduction for 2025 tax relief. For tax years 2025 through 2028, the OBBBA introduced a new deduction for seniors. Taxpayers reaching age 65 before the last day of the taxable year or older may claim an additional deduction of $6,000 per individual or $12,000 for a married couple where both spouses qualify. The additional deduction is available to taxpayers claiming either the standard deduction or itemized deductions. However, the senior deduction begins to phase out when MAGI exceeds $75,000 for single filers or $150,000 for joint filers. The deduction is completely phased out when MAGI reaches $175,000 for single filers or $250,000 for joint filers.

6. Take advantage of the new qualified tips deduction. As with the senior deduction, for tax years 2025 through 2028, employees and self-employed taxpayers may now deduct up to $25,000 of qualified tips received during the taxable year, regardless of whether the taxpayer itemizes their deductions or not. Regulations released by the IRS in late September provided a list of occupations that customarily receive tips and would be eligible for the deduction, along with rules as to what constitutes a “qualified” tip. For example, qualified tips must be voluntarily paid by the customer, so an automatic gratuity charge added to a customer’s bill will not qualify as a qualified tip for purposes of the deduction, as the customer did not have the option to not pay. The deduction is subject to phaseouts when MAGI reaches $150,000 for single taxpayers or $300,000 for married couples filing jointly.

7. Claim the new qualified overtime deduction. Effective for 2025 through 2028, eligible taxpayers may deduct up to $12,500 of qualified overtime (or $25,000 for married couples filing jointly). Qualified overtime is the portion of pay that exceeds their regular pay rate required by the Fair Labor Standards Act—effectively the “half” portion of “time-and-a-half” overtime compensation. Beginning for the 2026 tax year, employers and other payors will be required to file information returns with the IRS and Social Security Administration indicating the total qualifying overtime compensation for the year. For 2025, the portion of income that is qualified overtime earnings can be estimated by a reasonable method. For 2026, employers will need to track actual amounts of overtime paid and report it accordingly on 2026 wage and tax statements (Forms W-2). Just like the no tax on tips deduction, this deduction is available to both itemizing and nonitemizing taxpayers and is subject to phaseouts when MAGI reaches $150,000 for single taxpayers or $300,000 for married couples filing jointly.

8. Deduct car loan interest on the purchase of a new domestic car. Effective for 2025 through 2028, individuals may deduct interest paid on a loan used to purchase a qualified vehicle, provided the vehicle is purchased for personal use and meets other eligibility criteria. Lease payments do not qualify. The maximum annual deduction is $10,000, and phases out for taxpayers with MAGI over $100,000 ($200,000 for joint filers). In addition, the deduction is available for all taxpayers regardless of if they take the standard deduction or itemize.

To qualify for the deduction, the interest must be paid on a loan that is:

- Originated after December 31, 2024;

- Used to purchase a new vehicle originally used by the taxpayer and have its final assembly in the U.S.;

- For a personal use vehicle (not for business or commercial use); and

- Secured by a lien on the vehicle.

9. Utilize the new charitable deduction for nonitemizing taxpayers. Beginning in the 2026 tax year, a new deduction allows taxpayers to claim a deduction for charitable contributions worth up to $1,000 for single filers or $2,000 for married filing jointly. Only direct cash donations to eligible charities will qualify for purposes of this deduction; donations to donor-advised funds and private foundations and noncash donations do not qualify. This provision is permanent and is not indexed for inflation. The deduction is available to all taxpayers who do not itemize, regardless of income level.

We believe this new deduction will be reported as an “above the line” (and more favorable) deduction, reducing AGI. During the COVID pandemic, a similar deduction was available. For tax year 2020, the deduction was “above the line” and lowered AGI, though in 2021, the deduction was moved after the AGI calculation, following the standard or itemized deductions. We await IRS guidance to determine with certainty the location of this new deduction.

10. Turn losses into tax savings with the wagering losses deduction. In addition to being only able to deduct gambling losses to the extent of winnings, starting in 2026, you can only deduct at most 90 percent of your losses. This updated gambling loss rule is permanent.

Wagering Loss Deduction Illustration

|

Scenario |

2025 and Prior |

2026 and After |

|

Winnings: $100,000 |

Deduction: $100,000 |

Deduction: $90,000 |

|

Winnings: $90,000 |

Deduction: $80,000 |

Deduction: $72,000 |

|

Winnings: $40,000 |

Deduction: $40,000 |

Deduction: $40,000 |

For professional gamblers, the wagering loss deduction (subject to the same 90 percent limitation) can be claimed directly on a Schedule C (Profit or Loss from Business) along with their gambling income. Even though the deductions on the Schedule C will not be subject to the same itemized deduction limitations of a recreational gambler, they will likely still recognize phantom taxable income due to the 90 percent loss limitation, if their losses do not exceed 111 percent of winnings.

11. Plan ahead for new permanent and rolling qualified opportunity zones (QOZ) in 2027. The OBBBA permanently extended and modernized the QOZ program, originally enacted under the TCJA. While the TCJA program was scheduled to expire after 2026, the OBBBA created a permanent and rolling framework beginning January 1, 2027. As a result, careful timing is now critical when considering a QOZ investment, since different rules apply for 2025-2026 versus 2027 and later years.

Rules for 2025 and 2026: Under the TCJA rules, taxpayers could defer eligible capital gains by investing the gains in a qualified opportunity fund (QOF) within 180 days of realization. Deferred gains had to be recognized by December 31, 2026, with potential tax basis step-ups of 10 percent after five years and 15 percent after seven years.

Since the mandatory inclusion date of December 31, 2026, arrives before those holding periods can be satisfied, only investments made before 2021 could achieve a tax basis step-up. Any investments made after 2021 benefit only from temporary deferral until 2026. For 2025 investments, that translates to roughly a one-year deferral; no meaningful benefit remains for 2026 investments. However, both 2025 and 2026 would still benefit from an election to increase basis in the QOF investment to fair market value if held for 10 years or until 2047.

Rules for 2027 and future years: Beginning January 1, 2027, the OBBBA establishes a permanent, rolling opportunity zone program. Zones are now subject to decennial redesignation, with the first new determination date of July 1, 2026, and redesignations occurring every 10 years thereafter (July 1, 2036; 2046; etc.). Each new designation becomes effective on January 1 of the following year and remains in force for 10 years.

Under the new rules:

- Deferred gain is recognized at the earlier of a sale/exchange or five years after investment.

- If the investment is held five years, the basis increases by 10 percent of the deferred gain.

- If the investment is held 10 years, the basis equals the fair market value at sale—or automatically equals fair market value after 30 years if still held—eliminating post-investment appreciation from federal tax up to that 30-year mark. However, any appreciation occurring after the 30-year automatic step-up will be subject to capital gains tax when the investment is ultimately sold.

Qualified Opportunity Zone Rules by Year

|

Year of Investment |

2025 |

2026 |

2027 |

2027 |

|

Type of QOZ |

Normal QOZ |

Normal QOZ |

Normal QOZ |

Qualified rural opportunity zone |

|

Deferral Period |

Until Dec. 31, 2026 |

Until Dec. 31, 2026 |

Until earlier of sale/exchange or 5 years after investment |

Until earlier of sale/exchange or 5 years after investment |

|

Basis Adjustment After 5 Years (in Deferred Gain) |

Not applicable (cannot reach 5 years) |

Not applicable (cannot reach 5 years) |

10% of deferred gain ($100,000) |

30% of deferred gain ($300,000) |

|

Basis Adjustment After 7 Years (in Deferred Gain) |

Not applicable (cannot reach 7 years) |

Not applicable (cannot reach 7 years) |

Not applicable (no 7-year step-up under new rules) |

Not applicable (no 7-year step-up under new rules) |

|

Basis Adjustment After 10 Years (in QOF Investment) |

May elect fair market value basis until 2047 |

May elect fair market value basis until 2047 |

May elect fair market value basis for up to 30 years |

May elect fair market value basis for up to 30 years |

|

Deferred Gain Taxed |

Full $1,000,000 recognized in 2026 |

Full $1,000,000 recognized in 2026 |

$900,000 recognized in 2032 (after basis increase) |

$700,000 recognized in 2032 (after basis increase) |

12. Plant the seeds for your children’s future with “Trump accounts.” The OBBBA created a new savings account for children that will grow on a tax deferred basis, similar to a traditional IRA. For U.S. citizens born after December 31, 2024, and before January 1, 2029, establishing such an account will entitle the child to an initial $1,000 deposit from the government. Children born before or after this period are also eligible to set up these accounts as long as they are under 18 when they do so.

Parents, relatives and the children themselves can contribute up to an aggregated total $5,000 per year to the account, and employers may make an annual contribution of up to $2,500 to an account (which will not be included in the employee’s taxable income). The one-time $1,000 from the government does not count toward the yearly $5,000 limit, but employer contributions will reduce the annual limit. Contributions can be made until December 31 of the year they turn 18. These accounts are expected to be made available on July 4, 2026, and must be invested in an S&P 500 or a similar index fund. Upon the beneficiary attaining 18 years of age, the account will convert into a traditional IRA and is subject to all traditional IRA rules, including the 10 percent penalty for early withdrawal before age 59½, subject to the traditional IRA exceptions.

13. Act fast to utilize energy credits and deductions. Under the OBBBA, the majority of energy credits have been terminated. Some deadlines have already passed and more are set to end at the end of 2025 and early 2026. Now may be your last chance to receive a credit for energy efficient home improvements and electric vehicles. See the table below for important dates for taking advantage of energy credits before they expire.

Expiring Energy Credits

|

Credit |

Description |

New Sunset Date of Credit |

Planning Takeaways |

|

Clean vehicle credits |

A tax credit for individuals based on new and used vehicle purchases that are electric, plug-in hybrid and fuel cell. |

Vehicles must be acquired on or before September 30, 2025. |

N/A |

|

Credit for qualified commercial clean vehicles |

A tax credit for businesses purchasing clean vehicles for commercial use. |

Vehicles must be acquired on or before September 30, 2025. |

There is no limit on the number of credits your business can claim. For businesses, the credits are nonrefundable, so you can't get back more on the credit than you owe in taxes. |

|

Residential clean energy credit |

A tax credit for individuals for purchase of systems such as solar panels, wind turbines, battery storage and geothermal heat pumps. |

Qualifying expenditures (solar and water heating) must be made on or before December 31, 2025. |

Only applies to your main home or a second home that is not rented and located in the U.S. |

|

Energy efficient home improvement credit |

A tax credit for individuals for purchase of home improvement items such as windows, doors, insulation and hot water heaters. |

Eligible property must be placed in service on or before December 31, 2025. |

To qualify, building envelope components must have an expected lifespan of at least 5 years. This credit also includes labor costs for the installation. |

|

Alternative fuel vehicle refueling property credit (personal) |

A tax credit for individuals for purchase of electric vehicle chargers installed in your home. |

Eligible property must be placed in service on or before June 30, 2026. |

Install qualifying EV charging equipment before June 30, 2026, as long as you are located in eligible census tract (usually rural or low-income areas). |

|

Alternative fuel vehicle refueling property credit (business) |

A tax credit for businesses for purchase of electric vehicle chargers installed at a business or organization. |

Eligible property must be placed in service on or before June 30, 2026. |

Businesses and exempt organizations that meet prevailing wage and apprenticeship requirements are eligible for a 30% credit with a $100,000 per-item limit. |

|

Energy efficient commercial buildings deduction |

A tax deduction for commercial building owners purchasing interior lighting systems, heating/cooling, ventilation, and hot water systems. |

Eligible property must begin construction on or before June 30, 2026. |

Commence work before June 30, 2026, for significant tax savings. |

|

New energy efficient home credit |

A tax credit for eligible contractors who build or substantially reconstruct new, qualified energy-efficient homes, and own and have a basis in the home during construction, and then sell or lease it as a residence. |

Eligible property must be sold on or before June 30, 2026. |

Maximize your credit and sell a certified zero energy ready home. |

|

Clean electricity investment credit and clean electricity production credit |

A tax credit for businesses building and operating qualified facilities and energy storage technology. |

Solar and wind facilities must be placed in service on or before December 31, 2027, unless construction begins with 12 months of enactment of the OBBBA. Other types of energy facilities, such as nuclear, hydro and fuel cell remain eligible through 2033. |

The taxpayer claiming the credit must own the facility. Taxpayers cannot claim both investment credit and production credit for the same facility. |

|

Clean fuel production credit |

A tax credit for fuel producing businesses. Fuel produced after December 31, 2025, must be exclusively derived from feedstock produced or grown in the United States, Mexico or Canada. |

Extended through December 31, 2029. |

The maximum credit is $1 per gallon for nonaviation fuel and $1.75 per gallon for sustainable aviation fuel if all requirements are met. |

14. Claim 100 percent bonus depreciation on qualified production property (QPP). The OBBBA creates a new category of depreciable property known as QPP, which is eligible for 100 percent bonus depreciation.

QPP is generally nonresidential real property that is integral to a qualified production activity such as manufacturing, production or refining, resulting in a substantial transformation of a qualified product. In order to qualify for the 100 percent bonus depreciation, the construction must begin sometime between January 20, 2025, and December 31, 2028, and must be placed in service before January 1, 2031.

This new category of fixed assets creates an incentive to build manufacturing facilities in the United States. The incentive works by allowing the immediate deduction of certain real property (i.e., things like buildings and structures that are not movable) that otherwise would be depreciable evenly over 39 years.

Prior to the OBBBA, only limited types of real property known as qualified improvement property (QIP) were eligible for bonus depreciation. This includes interior improvements such as drywall, plumbing, electrical wiring, etc. that are added after a building has already been placed in service. Assets that are not considered QIP include enlargements/expansion and modifications to the internal structural framework of a building. QIP also specifically excludes elevators and escalators. QPP now makes up for this by essentially including everything that QIP excludes if it is an integral part of a qualified production activity.

Due to the expansion of bonus depreciation to QPP, taxpayers may want to consider the benefits of a cost segregation study when constructing a new multiuse facility where a portion of the activity will be devoted to qualified production activity. See strategy 98.

15. Turn year-end purchases into major tax savings with 100 percent bonus depreciation. In addition to QPP, the OBBBA has also permanently restored bonus depreciation to 100 percent of qualified new or used property placed in service after January 19, 2025. Bonus depreciation generally applies to qualified tangible personal property with a recovery period of 20 years or less (such as machinery, equipment, vehicles, computer equipment, office furniture and fixtures). Under the TCJA, bonus depreciation was scheduled to drop to 40 percent of qualified new or used property for 2025, which is still the case for property placed in service between January 1, 2025, and January 19, 2025.

|

Tax Year |

Bonus Depreciation Percentage |

|

2018-2022 |

100% |

|

2023 |

80% |

|

2024 |

60% |

|

January 1, 2025 – January 19, 2025 |

40% |

|

January 20, 2025, and thereafter |

100% |

16. Maximize corporate giving impact by contributing before year-end. In addition to the charitable floor for individual taxpayers discussed in strategy 1, the OBBBA also introduced a new 1 percent floor on charitable contribution deductions for corporations. Starting with the 2026 tax year, the new law provides that corporate taxpayers may claim a charitable deduction only to the extent that its charitable contributions exceed 1 percent of its taxable income.

17. Save on compliance expenses thanks to increased 1099 reporting thresholds. Forms 1099-MISC and 1099-NEC have long remained at a reporting threshold of $600, but that is set to change in 2026. For 2026, the OBBBA has increased the threshold to $2,000 for all qualified payments. Additionally, for calendar years after 2026 the threshold is indexed to increase for inflation.

18. Learn how new Form 1099-K rules affect your app-based income. For users of Venmo, PayPal, CashApp, Uber, DoorDash, Airbnb and similar apps, many taxpayers received Forms 1099-K for the first time with respect to the 2024 tax year as the threshold for Form 1099-K reporting was $5,000. This threshold was set to be further reduced to $2,500 in 2025, but the OBBBA retroactively set the threshold back to $20,000 in gross payments made over more than 200 transactions for transactions to a payee. This retroactive change applies to calendar year 2025 and onward and specifically applies to payments received through a third-party settlement organization. Excluded from this threshold are payments received through payment card transactions. Therefore, any payment received via credit cards, debit cards and store-value cards should produce a related Form 1099-K, regardless of the amount.

19. Claim a deduction for casualty and disaster losses. Thus far in 2025, there have been at least 115 federally declared natural disasters in the United States. A few examples include severe storms and flooding in Texas, Alaska and North Dakota, as well as tropical storms in North Carolina.

Prior to the TCJA, taxpayers were essentially able to deduct all personal casualty and theft losses as an itemized deduction. The TCJA restricted it so that such losses can only be deducted if they are attributable to a federally declared natural disaster, with limited exceptions. The original provision in the TCJA was temporary and was scheduled to sunset after 2025. The OBBBA made this permanent and expanded it to also include state declared disasters beginning in tax year 2026.

20. Prepare for 2026 opportunity zone gain recognition. Since 2018, taxpayers have had the option to defer the capital gains by reinvesting those gains into a QOF within 180 days of the sale. Under the TCJA opportunity zone rules, gains invested in QOFs are deferred until the QOF investment is sold or until December 31, 2026, whichever occurs earlier. For many taxpayers, large, deferred gains will be recognizable starting in 2026.

As mentioned in strategy 11, the deferred gains were allowed basis step-ups of 10 percent if held for five years and 15 percent if held for seven years. While the opportunity to take advantage of this basis increase has passed, investing in a QOF in 2025 still provides taxpayers the opportunity to defer capital gains until December 31, 2026, or until the investment is sold, whichever event occurs first. In addition, tax on the appreciation of the QOF may be avoided if the investment is held for over 10 years.

All 50 states have communities that now qualify for QOF investment plans. Besides investing in a fund, taxpayers may also take advantage of this opportunity by establishing a business in the QOZ or by investing in QOZ property.

21. Review new student loan rules and repayment options under the OBBBA. Beginning July 1, 2026, the OBBBA restructures federal lending and repayment programs. OBBBA replaces the current income-driven repayment plans with a new Repayment Assistance Plan (RAP), terminates Grad PLUS loans, establishes new annual and aggregate borrowing limits for Federal Direct Unsubsidized Stafford Loans for graduate and professional students and imposes new annual and aggregate limits on Parent PLUS borrowing per dependent student.

22. Consider withdrawing erroneous employee retention credit claims. The employee retention credit (ERC) was introduced to taxpayers during COVID-19, incentivizing businesses who keep employees on their payroll during times of economic turmoil with the opportunity to receive the credit. This credit saw widespread fraud by third-party promoters encouraging ineligible businesses to file improper ERC claims. In response to the surge in fraudulent ERC claims over the years, the IRS has increased enforcement, using the additional funding from the Inflation Reduction Act of 2022 to hire and train employees on investigating abuses of this credit. This resulted in several lawsuits against these unscrupulous promotors, both by the IRS and their clients. Any business with a pending ERC claim that they subsequently realized was ineligible can voluntarily withdraw the claim as long as the following conditions are met:

- An amended employment tax return was filed to claim the ERC (Forms 941-X, 943-X, 944-X, CT-1X).

- The amended return has no other changes besides claiming the ERC.

- The withdrawal is for the entire amount of the ERC claim for the quarter.

- If the IRS has already processed the returns and paid the claim, the refund checks have not been received, cashed or deposited.

Once the withdrawal is filed, the IRS will send a letter stating whether the withdrawal request was accepted or rejected. Without the acceptance letter, the withdrawal request is not considered completed. If the withdrawal is accepted, an amended income tax return may be needed.

Interestingly, the OBBBA has extended the government’s statute of limitations to assess ERCs filed for the third and fourth quarters of 2021. For these periods, the IRS’ limitations period was extended to five years under the American Rescue Plan Act of 2021, rather than the normal three years the IRS has to assess tax. The OBBBA further extended the period to six years from the date the original return was filed or the date the ERC claim was filed, whichever is later.

In addition, the IRS is now statutorily prohibited from allowing or refunding any ERCs for the third and fourth quarters of 2021 that were filed after January 31, 2024, even if all eligibility requirements have been met. The OBBBA has also tightened restrictions on ERC promoters by imposing fines and penalties on promoters who failed to satisfy all due diligence requirements.

If you filed ERCs before the January 31, 2024, cutoff and still receive Letter 105-C, Claim Disallowed, you have the right to appeal to the IRS Independent Office of Appeals. Additional information on how to respond with an appeal can be found on the IRS website.

Nearly all cash-basis taxpayers can benefit from strategies that accelerate deductions or defer income, since it is generally better to pay taxes later rather than sooner (especially if income tax rates are not scheduled to increase). For example, a check you send in 2025 generally qualifies as a payment in 2025, even if it is not cashed or charged against your account until 2026. Similarly, deductible expenses paid by credit card are not deductible when you pay the credit card bill (for instance, in 2026), but when the charge is made (for instance, in 2025).

With respect to income deferral, cash-basis businesses, for example, can delay year-end billings so that they fall in the following year or accelerate business expenditures into the current year. On the investment side, income from short-term (i.e., maturity of one year or less) obligations like Treasury bills and short-term certificates of deposit is not recognized until maturity, so purchases of such investments in 2025 will push taxability of such income into 2026. For a wage earner (excluding an employee-shareholder of an S corporation with a 50 percent or greater ownership interest) who is fortunate enough to be expecting a bonus, he or she may be able to arrange with their employer to defer the bonus (and tax liability for it) until 2026. However, if any of this income becomes available to the wage earner, whether or not cash is actually received, the bonus will be taxable in 2025. This is known as the constructive receipt doctrine.

23. Defer income until 2026 to take advantage of inflation adjustments to tax brackets. For 2025, the top individual tax rate remains 37 percent and is applied to joint filers with taxable income greater than $751,600 and single filers with taxable income greater than $626,350. More importantly, for 2026, the OBBBA preserved these brackets enacted under the TCJA and made them permanent. The thresholds for the top 37 percent bracket will rise in 2026 to $768,700 for joint filers and $640,600 for single filers. It might be advantageous for many taxpayers to accelerate their deductions into 2025, reducing their potential tax liability this year. Additionally, for those who are able, taxpayers should plan to defer income into 2026 to take full advantage of the threshold increases to the tax brackets. While there are many ways to defer your income, waiting to recognize capital gains or exercise stock options are popular options that would not only lower your investment income, but your taxable income as well. Depending on your situation, these strategies could reduce tax due for 2025 and potentially 2026 as well.

2025 and 2026 Federal Tax Brackets

|

Tax Rate |

Single – 2025 |

Single – 2026 |

Married Filing Jointly – 2025 |

Married Filing Jointly – 2026 |

|

10% |

$0 – $11,925 |

$0 – $12,400 |

$0 – $23,850 |

$0 – $24,800 |

|

12% |

$11,926 – $48,475 |

$12,401 – $50,400 |

$23,851 – $96,950 |

$24,801 – $100,800 |

|

22% |

$48,476 – $103,350 |

$50,401 – $105,700 |

$96,951 – $206,700 |

$100,801 – $211,400 |

|

24% |

$103,351 – $197,300 |

$105,701 – $201,775 |

$206,701 – $394,600 |

$211,401 – $403,550 |

|

32% |

$197,301 – $250,525 |

$201,776 – $256,225 |

$394,601 – $501,050 |

$403,551 – $512,450 |

|

35% |

$250,526 – $626,350 |

$256,226 – $640,600 |

$501,051 – $751,600 |

$512,451 – $768,700 |

|

37% |

Over $626,350 |

Over $640,600 |

Over $751,600 |

Over $768,700 |

24. Be aware of the increased standard deduction. As a result of the OBBBA, the increased standard deduction taxpayers enjoyed over the past seven years has been permanently extended and indexed for inflation so that the 2025 standard deduction is $31,500 for a joint return (an increase of $2,300) and $15,750 for a single return (an increase of $1,150). Taxpayers 65 years or older and those with certain disabilities may claim additional standard deductions, including the new senior deduction discussed in strategy 5.

|

Standard Deduction (based on filing status) |

2024 |

2025 |

|

Married filing jointly |

$29,200 |

$31,500 |

|

Head of household |

$21,900 |

$23,625 |

|

Single (including married filing separately) |

$14,600 |

$15,750 |

25. Weigh the pros and cons of filing separately this year. A great majority of the time, it is more advantageous for a married couple to file a joint return as opposed to filing separately. However, there are limited circumstances where it may be more beneficial to file separately, such as when one spouse does not want to be responsible for the other’s tax debts, when student loan repayments can be reduced under an Income-Driven Repayment Plan (see strategy 21), where there is a concern about accuracy or completeness of the other spouse’s tax information or to avoid a “marriage penalty.” A marriage penalty occurs typically when both spouses have relatively high income but are still individually within the lower brackets so that the effective tax rate on their income is less when filing separately than it is when filing jointly. This scenario only occurs in very limited circumstances—when both spouses’ individual income amounts fall within the exact right area.

Conversely, many tax deductions and credits are completely disallowed for taxpayers married filing separately, including:

- The child and dependent care credit;

- The earned income credit;

- The credit for the elderly and disabled;

- The “American opportunity” credit;

- The lifetime learning credit;

- The credit for adoption expenses;

- The student loan interest deduction;

- The new $6,000 deduction for seniors over the age of 65;

- The new no tax on tips deduction; and

- The new no tax on overtime deduction.

Further, the mortgage debt limit for which a taxpayer can deduct mortgage interest as an itemized deduction is cut in half for a taxpayer that is married filing separately. Also, keep in mind that if filing separately and one spouse elects to itemize their deductions instead of taking the standard deduction, the other spouse must also itemize their deductions even if in total they are less than the standard deduction.

If you do intend to file separately for a nontax reason, make sure you communicate that intention to your tax return preparer. In most cases, your tax preparer will analyze which filing status creates optimal tax results and discuss advantages and disadvantages of each filing status.